Investors are ramping up their positions in the cannabis industry, as expanded legalization in new U.S. states and the launch in late 2018 of Canada’s adult-use market open new opportunities.

Key nuances that point to important shifts in industry trends are emerging with each deal that gets signed.

Here are the top takeaways, insights and analysis on key mergers & acquisitions from the first quarter.

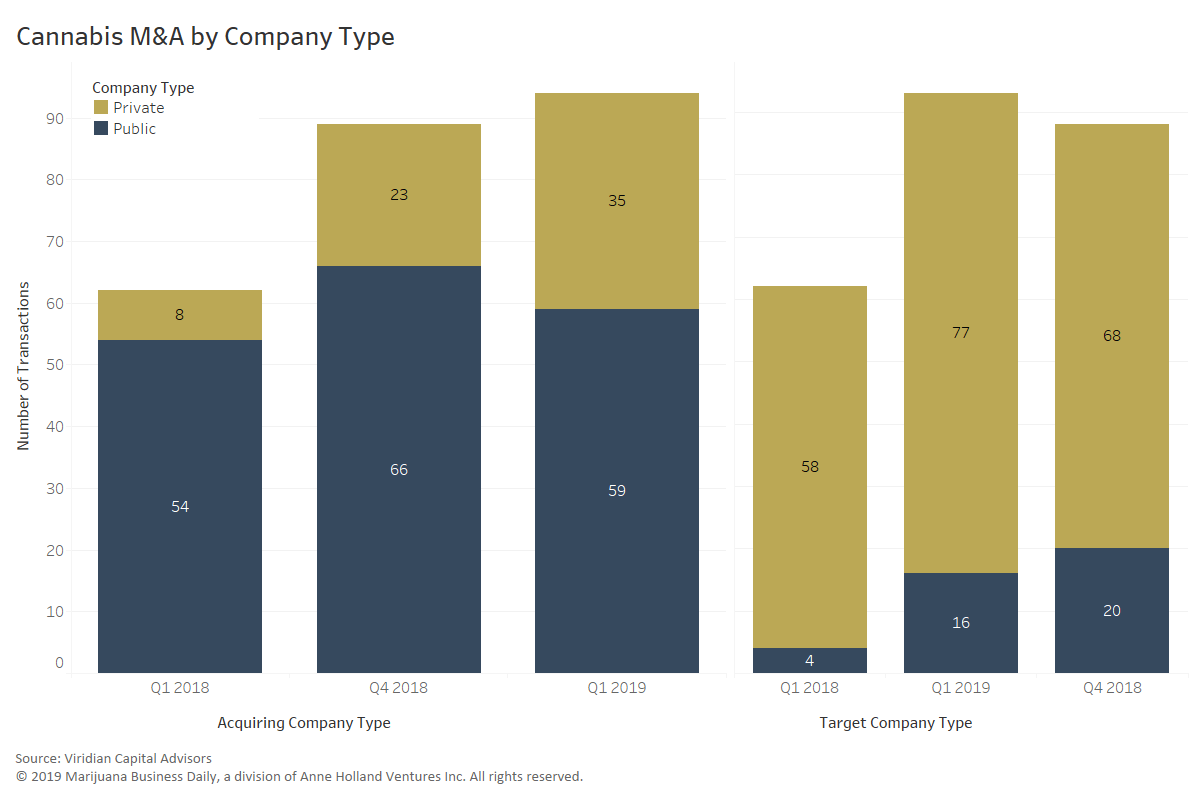

By the Numbers

Nearly 100 mergers and acquisitions were inked in the first quarter, up more than 51% from the same period in 2018 when 62 deals closed.

The sectors below are unchanged from those that led M&A activity in 2018, signifying the continuation of major cannabis trends from 2018 into 2019.

Sectors Leading the Way: Buyers

1. Cultivation & Retail: 37 deals

The primary drivers of M&A activity by buyers in the Cultivation & Retail sector are the consolidation of growers and retailers in existing markets, operators branching into new markets (U.S. states or other nations) and companies acquiring new business lines or product/service offerings outside of the sector.

2. Investments/M&A: 13 deals

M&A activity of acquirers in the Investments/M&A sector reflects varied strategies pursuant to the acquiring firms’ mandates. This has led to a wide breadth of structures and initiatives seeking to capitalize on all sectors of the cannabis industry.

3. Infused Products & Extracts: 11 deals

Infused Products & Extracts companies have typically sought to acquire brands for their portfolios, to expand their operations into new jurisdictions or to acquire a valuable infusion or extraction technology. Companies in this sector have also looked to acquire in the Cultivation & Retail sector to lock in a source of raw cannabis flower inputs or capture margin by pursing vertical integration.

Sectors Leading the Way: Targets

1. Cultivation & Retail: 28 transactions

Cultivation & Retail companies – the core of the cannabis industry – have been the primary targets of acquisitions. Most of the acquiring companies targeting this space have been from the Cultivation & Retail and Investments/M&A sectors.

Primary strategies for acquiring Cultivation & Retail companies include consolidating within existing and maturing markets and establishing operations in new jurisdictions (U.S. companies getting around the ban on interstate commerce and Canadian firms buying into other nations) to capture additional demand or lock in low-cost supply.

2. Non-Cannabis-Related: 19 transactions

The majority of acquisitions of Non-Cannabis-Related companies have related to reverse takeover and reverse merger going-public transactions. Initially, these transactions were mostly completed by Canadian cannabis licensees seeking public listings, but more recently, American MSOs and Infused Product & Extracts companies have moved to the public markets via reverse mergers/takeovers.

Outside of the going-public transactions, Non-Cannabis-Related companies have been acquired by companies in the industry looking to add cannabis or hemp/CBD to their existing capabilities (e.g., acquiring a coffee company to begin infusing it with cannabinoids.

3. Infused Products & Extracts: 14 transactions

The main sectors targeting companies in the Infused Products & Extracts sector are Cultivation & Retail, Investments/M&A and Infused Products & Extracts.

Cultivation & Retail companies have bought into this sector to capture additional value by branching into the extraction space as well as to add branded products to their catalogs. Infused Products & Extracts companies have acquired others in the same sector to add new brands or products to their portfolios, to establish operations in new jurisdictions and to capture new technologies around extraction and infusion. Investments/M&A firms have acquired Infused Products & Extracts companies for a variety of purposes, most of which follow those mentioned above.

Of Note – Hemp: 12 transactions

Interest in hemp and CBD companies has been growing since the beginning of 2018 because of the proliferation of state-legal hemp programs and the passage of the U.S. Farm Bill in December 2018. Acquirers of companies in the hemp sector are seeking to capitalize on this new, burgeoning piece of the overall cannabis industry because of its broad applications in health, wellness and consumer products.