Already struggling capital markets further tightened by the coronavirus, a declining stock price and an improving legalization outlook for cannabis have combined to derail five of the 10 planned deals in Schwazze’s strategy to consolidate the Colorado market.

While COVID-19 actually has improved the long-term investment case for the marijuana industry after state governments deemed it “essential,” the pandemic has made capital markets for cannabis even more skittish.

“(Schwazze) just didn’t raise the money in time, they didn’t have enough to close at the contract deadline, and we let it expire,” said Tim Cullen, founder and CEO of Colorado Harvest Co., which terminated its deal with the Denver company on June 1.

In a news release, Schwazze CEO Justin Dye reiterated plans to pursue a vertical-integration strategy within acceptable terms to shareholder return.

“We know that continuing to focus on shareholder return is the right thing to do at this time,” he noted. “Our board believes that it is in our best interest to build a differentiated business in Colorado.”

Avoiding deals that can be financed only on unacceptable terms is ultimately a positive for shareholders.

In addition, it might make sense for both buyers and sellers to sit tight and see how regulations change based on the current political climate and upcoming presidential election.

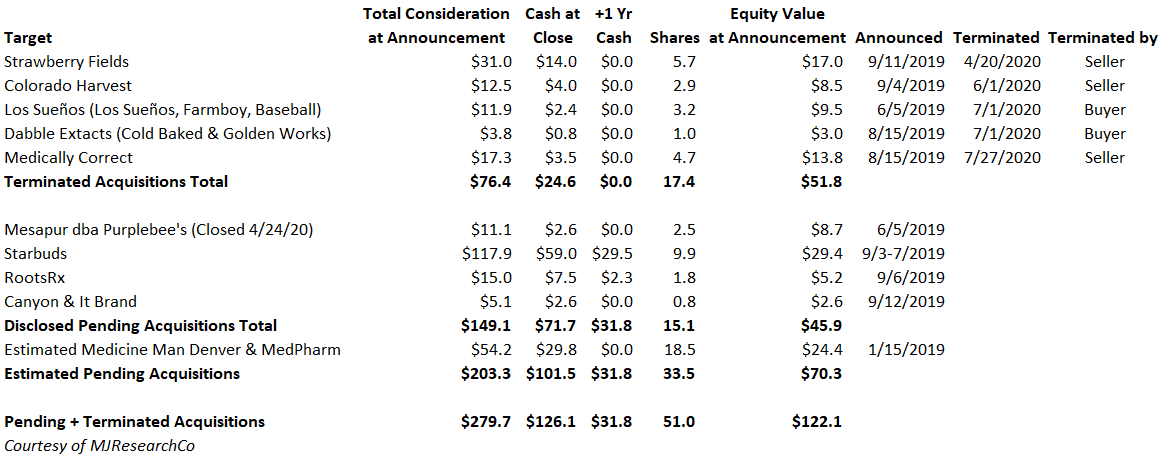

Schwazze needed to raise at least $96 million to close

As previously detailed in Marijuana Business Daily’s October 2019 Deep Dive on Schwazze (then called Medicine Man Technologies), the company announced 10 deals between January 2019 and September 2019 to consolidate its Colorado supply chain and build the largest vertically integrated operator in the state.

In October, we noted that “raising cash to close is the biggest risk; this all makes sense on paper, but the capital markets for cannabis stocks have tightened.”

This inability to raise the cash seems to indeed be the strategy’s undoing.

Schwazze needed at least $96 million in cash to close the acquisitions, excluding related-party transactions.

I estimate those transactions require another $30 million of cash.

They include Medicine Man Denver dispensaries and MedPharm cultivations (former CEO Andy Williams owns 38% and 29% of these, respectively, as well 2.2 million shares of Schwazze, per the company’s annual report).

Schwazze raised $20.0 million from Dye Capital in the year ended March 2020, but most of that was consumed through enhancing the company’s corporate infrastructure to consolidate the Colorado market.

Only the purchase of MesaPur, which required just $2.6 million of cash, has closed.

U.S. Securities and Exchange Commission filings indicate Schwazze terminated the Los Sueños and Dabble Extracts deals, citing “key business and valuation issues” identified in due diligence, while Strawberry Fields, Colorado Harvest and Medically Correct terminated their deals.

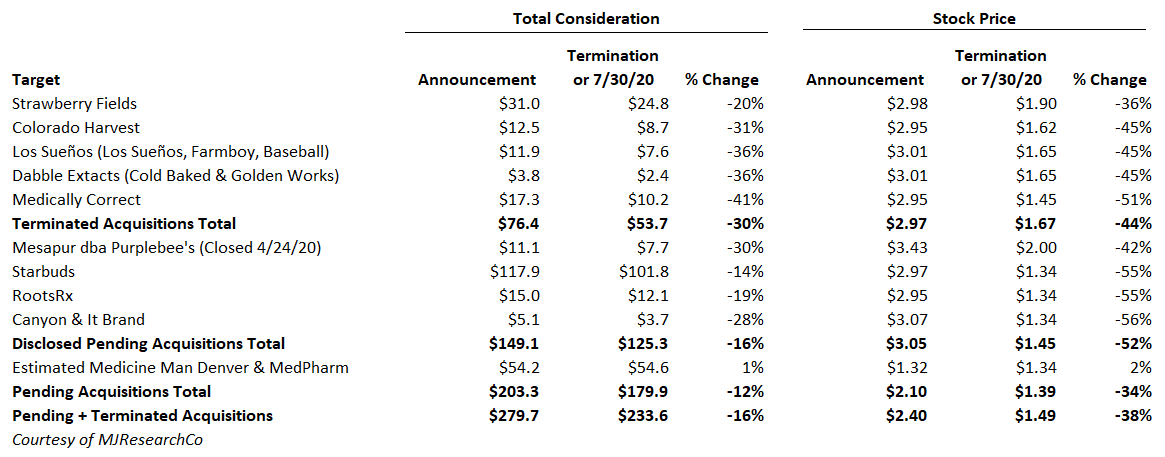

Consideration dropped with stock price while company operations surge

The value of the total consideration to be paid to close those transactions also declined by an average of 30%, the result of a 44% average decline in Schwazze’s shares, which reduced the value of the equity component. The company trades on the over-the-counter market as SHWZ.

When equity is involved in transactions, sellers that join to manage the newly combined company should focus more on the percentage of the combined company owned than on the headline value at either the announcement or the close.

This seems to be the case with the closed acquisition of MesaPur, since that company’s founder, Jim Parco, is continuing as the senior vice president of manufacturing for Schwazze.

But for sellers who do not plan to continue working with a merged company, it can be problematic to see overall consideration drop so drastically – especially if the underlying company operations are doing even better than expected and there are other potential suitors or operational plans.

$59 million cash needed last week for Starbuds

The failed deals required $25 million of cash, meaning Schwazze still needs to raise at least $72 million to close the unrelated transactions and an estimated $30 million more to close the related-party transactions.

The largest remaining deal is for Starbuds, which Schwazze reiterated in a June 8 SEC filing is on track.

Schwazze needed to provide Starbuds proof of $59 million in funds by July 30, 2020, or “such later date as mutually agreed by the parties.”

The lack of an announcement regarding success or failure as of press time implies that the parties agreed to extend the timeline.

The next-largest deal is for Medicine Man Denver and MedPharm, but given the related-party nature of the ownership, these transactions will be more complex to close – and we do not know the cash-versus-equity breakdown of the consideration.

Are these still the right targets?

For now, Schwazze is continuing to pursue Starbuds, Medicine Man Denver, MedPharm, RootsRx and Canyon Cultivation (and, presumably, the It brand), but there are many other Colorado operators that might be more willing to sell at different terms.

As Colorado Harvest’s Cullen noted: “We aren’t a distressed asset and don’t need to sell today.”

An executive for Schwazze was unavailable for comment because the company is entering its quiet period ahead of reporting second-quarter earnings in mid-August, when it will likely provide an update on the acquisition and funding strategies.

Schwazze’s original idea – to expand margins by consolidating a fragmented yet profitable market – remains a good one for companies that have both the integration skills and the capital to execute.

The know-how Schwazze’s management team gained in the grocery, food and airline industries should bring the integration skills. The capital might remain a challenge for the time being.

Schwazze’s experience just shows how capital intensive and capital constrained the cannabis industry currently is.

Mike Regan is the founder of MJResearchCo and a regular contributor to Marijuana Business Daily. He can be reached through his LinkedIn page or at info@mjresearchco.com.