Investors are ramping up their positions in the cannabis industry, as expanded legalization in new U.S. states and the launch in late 2018 of Canada’s adult-use market open new opportunities.

Key nuances that point to important shifts in industry trends are emerging with each deal that gets signed.

Here are the top takeaways, insights and analysis on key capital raises from the first quarter.

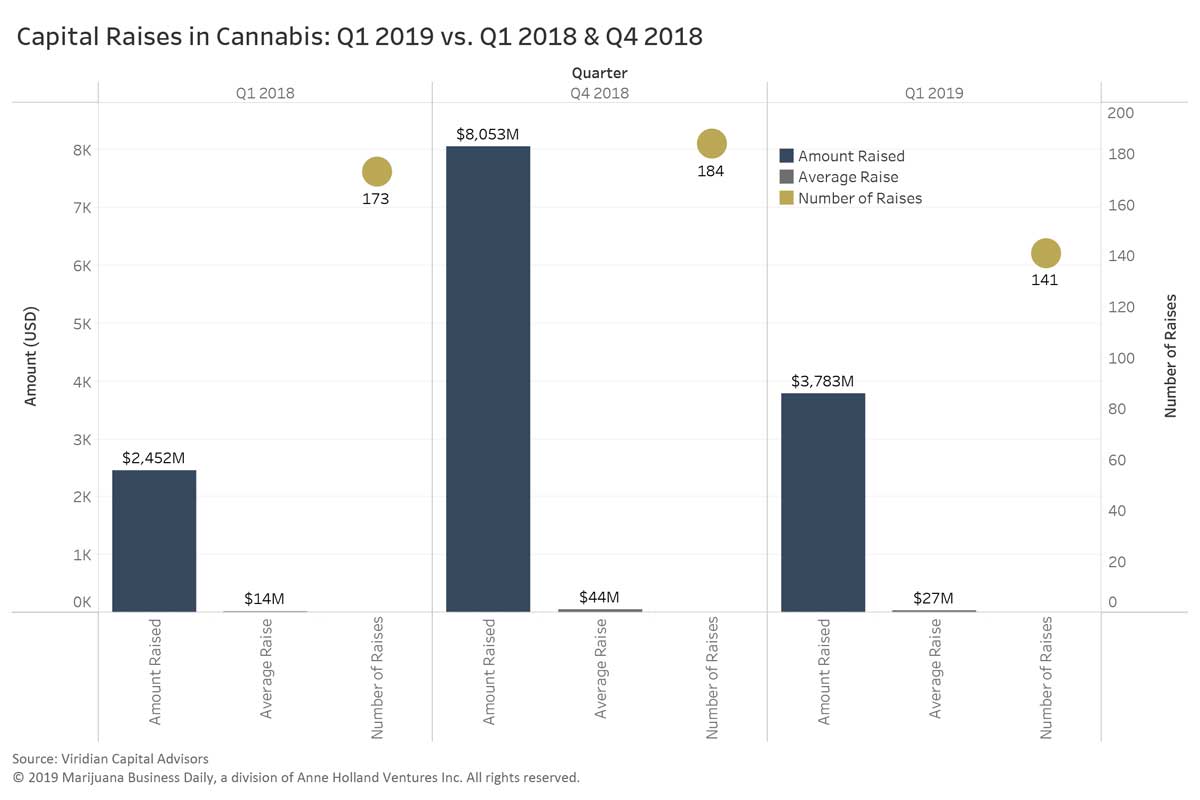

By the Numbers

Cannabis companies raised nearly $4 billion in the first quarter – that’s up more than 50% from the year-ago quarter, even with 18.5% fewer raises closed.

The quarter included liquor giant Altria Group’s $1.8 billion investment into Canada’s Cronos Group – a significant outlier when compared with other investments during the period. Excluding this deal, there would have been a reduction in capital raised year-over-year from Q1 2018 to Q1 2019.

Key drivers of this trend include concerns about valuations in the public markets, particularly related to supply constraints in the Canadian adult-use market.

Sectors Leading the Way

1. Cultivation & Retail: 63 raises totaling $3 billion (including the $1.3 billion Altria-Cronos raise)

The primary drivers for the Cultivation & Retail sector continue to be the progression of cannabis legalization across the United States with new medical and adult-use markets being launched as well as expansions of existing markets.

In the U.S., this sector has been boosted by the “land grab” strategy being deployed by more successful multistate operators as they consolidate their competitors, accumulate additional market share and expand into new jurisdictions.

In Canada, more developed licensed producers have been raising larger tranches of capital as they seek to expand their operations within Canada and move into newer cannabis markets internationally.

Similarly, MSOs in the U.S. have raised larger rounds, mainly to establish or acquire operations/assets in new states. Investments in this sector have focused on higher-value jurisdictions such as the adult-use markets in California, Nevada, Massachusetts and, now, Michigan as well as key medical markets such as Florida and Arizona.

2. Real Estate: Six raises totaling $278.2 million

Real estate investments in Q1 were few in number but significant in size with the average raise coming in at more than $46 million. These raises were mostly completed by cannabis-focused real estate investment trusts (REITs).

Recently, several MSOs, including MedMen and Acreage, have partnered with or established REITs to unlock the capital tied up in their real estate assets via sale-leaseback transactions. This trend is expected to continue until more traditional methods of unlocking this equity, such as mortgages, become more accessible to cannabis operators.

3. Investments/M&A: 16 raises totaling $128.6 million

Raises in the Investments/M&A sector have mostly tracked the overall growth of the cannabis space as investors target publicly traded holding companies, royalty or streaming companies, lenders and venture capital and private equity funds, among others. New firms in this sector continue arising and raising capital to fund their initial plans, whereas firms in the Investments/M&A sector that are a bit older and have been successful in their allocations are moving on to larger raises.

Of Note – Hemp: 10 raises totaling $71.4 million

Hemp companies have increasingly raised capital after the passage of the U.S. Farm Bill in December 2018. These businesses have sought rapid expansion to take advantage of the national and international opportunities in hemp but particularly cannabidiol (CBD) products that have garnered significant consumer interest.

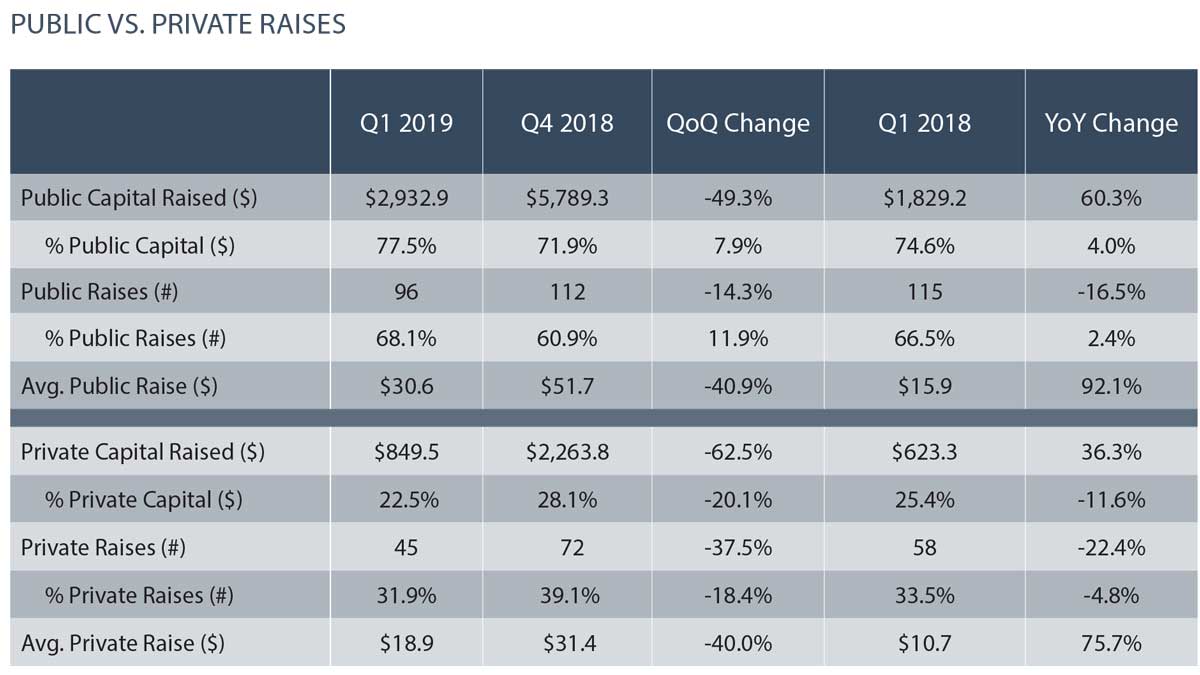

Public vs. Private Raises

Year-over-year

Public company raises increased 60.3% year-over-year from $1.8 billion in Q1 2018 to $2.9 billion in Q1 2019. This growth was accompanied by a decline in the number of raises – from 115 to 96, leading to a 90%-plus increase in the average raise size from $15.9 million to $30.6 million

Capital raised by private companies increased 36.3% year-over-year from $623 million in Q1 2018 to nearly $850 million in Q1 2019. This increase occurred with a 22.4% decline in the number of private raises, leading to an increase in average raise size of more than 75%.

This is in line with the steady maturation of the industry and its companies as consolidation and organic growth drive scale, necessitating larger rounds of capital to sustain expansion.

Quarter-over-quarter

Public company raises declined nearly 50% quarter-over-quarter from Q4 2018 to Q1 2019, spurred largely by valuation concerns and supply constraints in the Canadian adult-use market.

The reduction in capital raised by public companies was accompanied by a 14.3% reduction in the number of transactions.

When Constellation Brands’ and Altria’s investments are removed from the figures for Q4 2018 and Q1 2019, respectively, the capital raised by public companies falls to $1.2 billion in Q1 2019 and $1.9 billion in Q4 2018.

With the outlier raises removed, capital raised by public companies fell 38.9% quarter-over-quarter. Again, this reduction stemmed largely from concerns around valuations and supply constraints in the Canadian adult-use market.

Private company raises declined nearly 63% quarter-over-quarter from Q4 2018 to Q1 2019, mostly driven by a reduction in large U.S. multistate operators undertaking significant pre-RTO raises that totaled more than $1 billion in Q4 2018.

We have seen a shift of interest toward private companies, particularly those in the United States, as investors move away from publicly traded firms and those in Canada that had previously garnered the most interest.

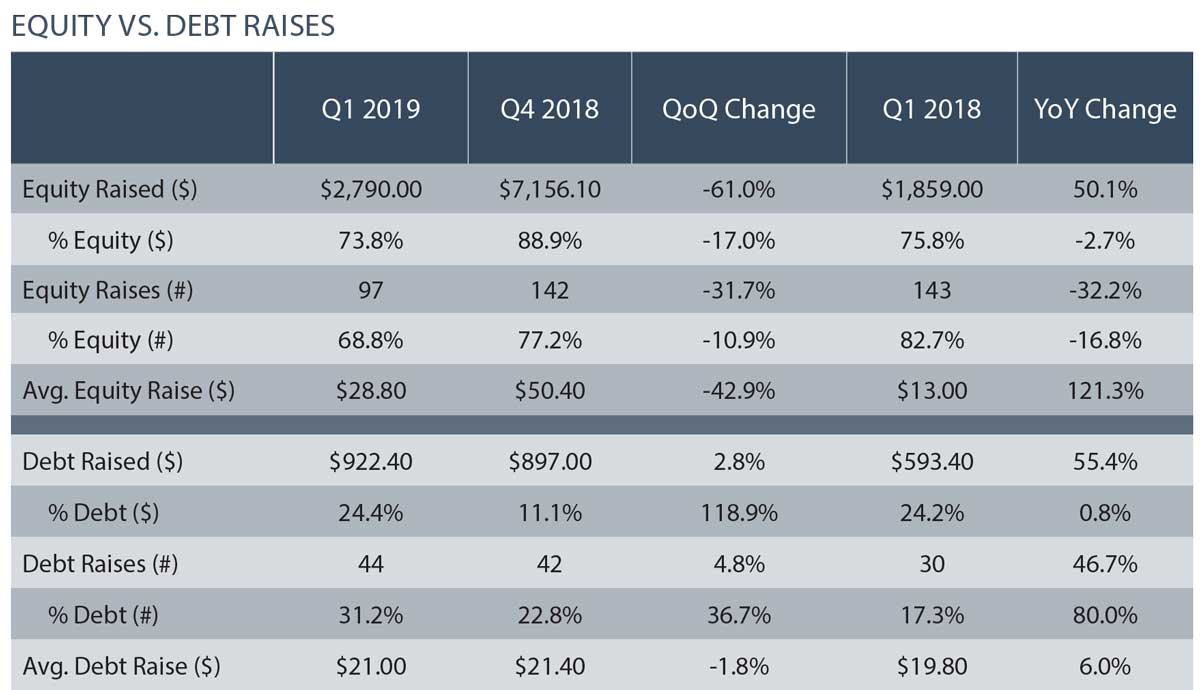

Equity vs. Debt

Year-over-year

Equity raises increased 50.1% year-over-year from $1.9 billion in Q1 2018 to $2.8 billion in Q1 2019. This growth was accompanied by a decline in the number of raises – from 143 to 97. That represents a more than 120% increase in the average raise size – from $13 million to $28.8 million.

Removing the Altria-Cronos investment from the Q1 data decreases the capital raised using equity structures to $1 billion, a 44.9% decline from the $1.8 billion raised in that manner in Q1 2018. Without the Altria-Cronos raise, the average equity raise declined, too, from $13 million to $10.7 million.

Again, this reduction primarily stems from the shift away from publicly traded companies that have mostly raised capital through equity structures.

Debt capital raised, the number of debt raises and the average debt raise size all increased year-over-year from Q1 2018 to Q1 2019. There has been a steady increase in the use of debt structures in the industry as asset bases have expanded, cash flows and financial performance have improved, and operating histories have lengthened.

Expanded debt offerings are expected on the horizon, especially for larger companies with more significant asset bases. Additionally, access to banking services and products in the United States should expand more traditional financing options, including mortgages and small business loans, for cannabis businesses.

Quarter-over-quarter

Equity raises declined 61% from Q4 2018 to Q1 2019, accompanied by reductions in both the number of raises and average raise size. Without the Constellation-Canopy and Altria-Cronos raises, there was a 50.4% reduction in equity capital raises over these two quarters.

The reduced capital raised using equity structures was mostly driven by lower capital raise activity by public companies in the cannabis industry.

Debt capital raised rose 2.8% quarter over quarter, and the proportion of total debt capital raised in the industry more than doubled to 11.1% from Q4 2018 to Q1 2019. Larger producers and MSOs are increasingly raising debt capital – including convertible debt – as longer operational histories, increasing operating cash flows and larger asset bases give lenders greater comfort in providing capital to these businesses.