As the recreational marijuana industry expands and matures, branding will be a vital strategy for companies vying for market share.

Companies that build identities that resonate with consumers while fulfilling their needs will continue to grow – even once the industry’s rapid expansion eventually slows.

Building brands that connect to buyers takes time. But that work is already paying off for some companies in California, Colorado and Washington state.

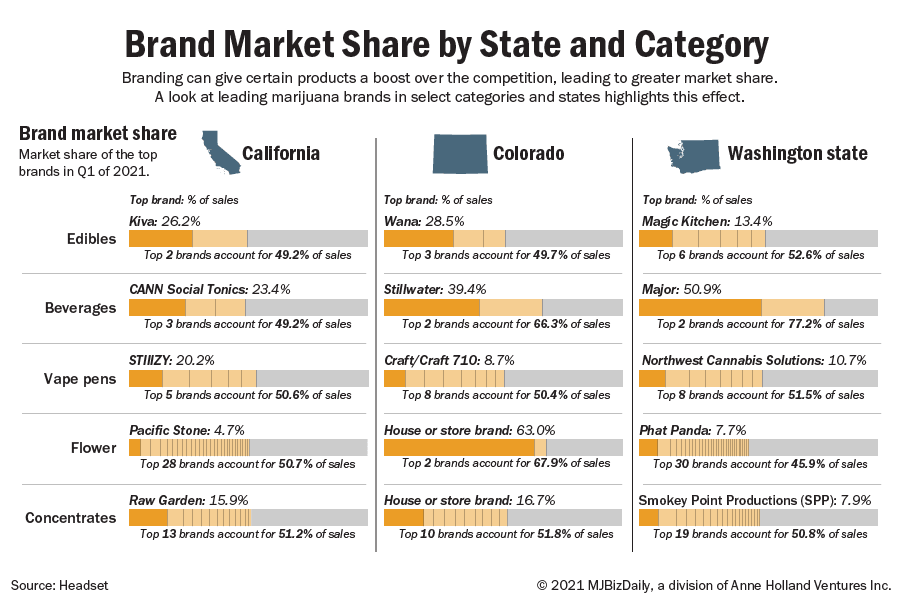

Analysis of first-quarter market share data provided by marijuana analytics firm Headset shows some clear winners, particularly in consumer packaged goods categories such as edibles and beverages.

While these segments don’t have the overall market share that flower does, they tended to be dominated by fewer brands when compared to flower in the states analyzed.

Beverage sales are dominated by two or three brands, which are often responsible for 50% or more of the sales in a state.

The top two beverage brands in Washington state make up 77.2% of sales, led by Major, a local brand launched in 2019, which accounted for 50.9% of that state’s beverage sales in the first quarter of 2021.

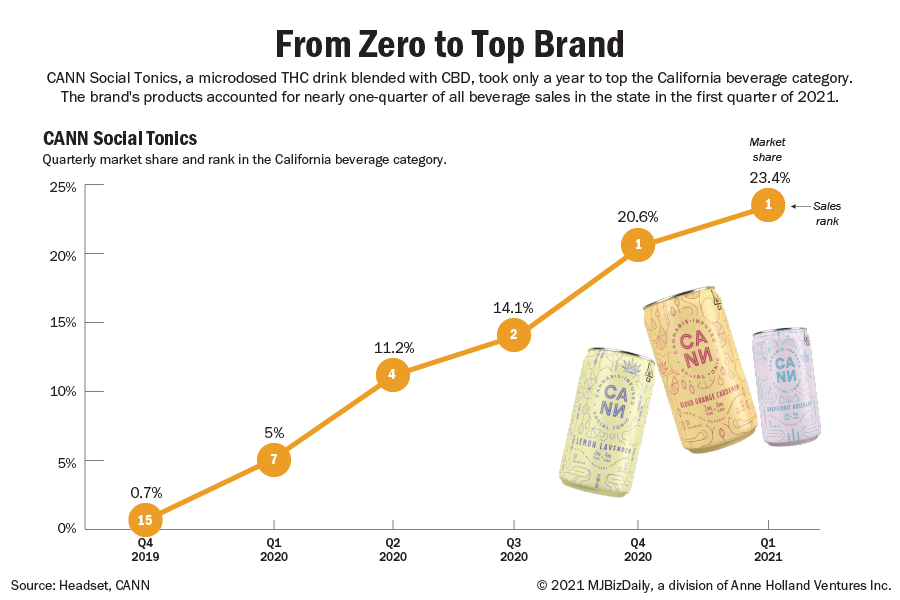

Stillwater in Colorado led beverage sales in the first quarter with 39.4% of sales, while Cann Social Tonics pulled in 23.4% of sales in California.

Introduced in 2019 as a microdosed THC drink blended with CBD, Cann Social Tonics climbed into the top beverage brand spot in California in about a year.

The company entered the market with less than 0.1% of category sales, ranking it 15th. But by the fourth quarter of 2020 it had attained 20.6% of the beverage market.

This highlights there is plenty of room for market disruption from sophisticated brands that meet the needs of consumers.

In this case, a marijuana-infused drink marketed as a “light and uplifting buzz” found its target.

The top brands in other categories, such as concentrates, flower and vape, often are more spread out between brands.

In California, 28 brands accounted for the top 50.7% of flower sales compared to two brands making up 49.2% of edible sales.

The flower category also has added competition from house or store brands in many markets.

For example, house brands were responsible for 63% of flower sales in Colorado for the first quarter of this year.

But some regional brands have pushed through.

Pacific Stone in California topped flower brands in the state with 4.7% of sales in the first quarter.

Some states, like Washington, don’t permit house brands, allowing Phat Panda to top the flower market there with with 7.7% of flower sales.

Top brands have a bit more market share in the concentrates and vape categories, but rarely attain more than 15% of sales.

The STIIIZY vape brand is the exception, topping the California vape market with 20.2% of sales.

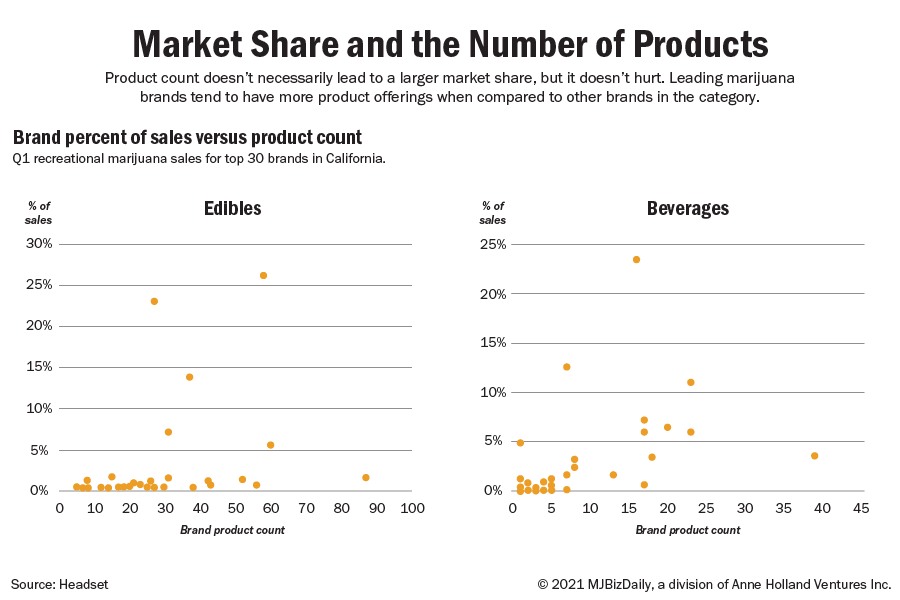

One way to expand a brand’s dominance in a category is to expand the product offerings within the category.

Product count doesn’t necessarily lead to a larger market share, but it doesn’t hurt.

In the analysis of the three states, leading marijuana brands tended to have more product offerings when compared to other brands in the category.

But there are outliers.

Uncle Arnie’s Iced Tea Lemonade is a one product brand in California that brought in 5% of the total first-quarter sales for beverages in the state.

In contrast, Cannavis Syrup brand had 39 SKUs in the same time period and accounted for 3.6% of total sales.

Market-leading Cann Social Tonic had 16 products.

Andrew Long can be reached at andrew.long@mjbizdaily.com.