Colorado’s retail marijuana sector has seen more consolidation as it’s matured, but relative to more established industries, it remains a highly competitive and open market.

It’s a reminder that the dust has yet to settle in the nation’s most developed legal marijuana market – and there will likely be far more consolidation in the years ahead.

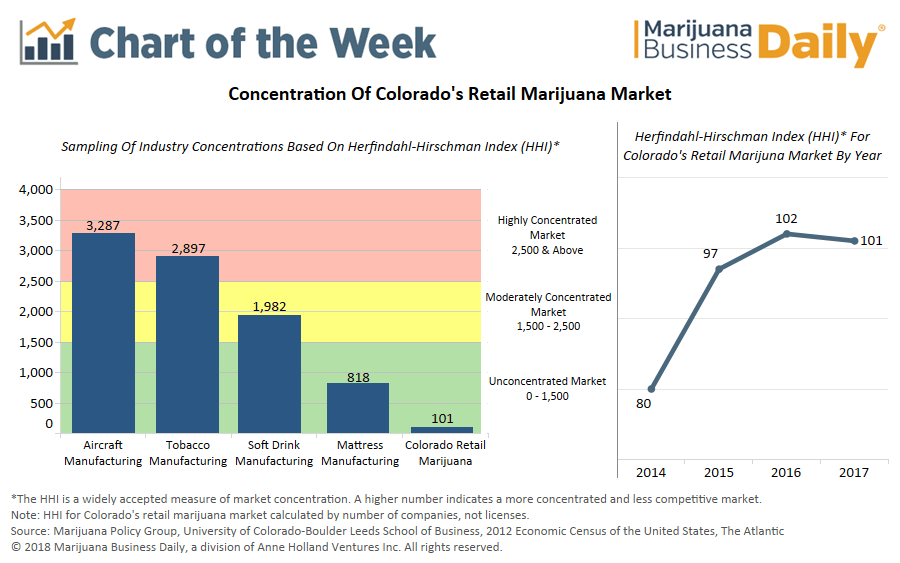

In a joint report from the Denver-based Marijuana Policy Group and the University of Colorado Leeds School of Business, researchers combined sales data from the state’s marijuana inventory tracking system (Metrc) with the number of licensed retail businesses in Colorado, allowing them to measure the level of competition and consolidation within the sector.

That measurement – known as the Herfindahl–Hirschman Index (HHI) – is a widely accepted metric used by the U.S. Department of Justice and the Federal Trade Commission to determine the effects of mergers and acquisitions on an industry.

Based on the HHI, markets are generally classified into three types:

- Unconcentrated (HHI below 1,500)

- Moderately concentrated (HHI between 1,500 and 2,500)

- Highly concentrated (HHI above 2,500)

In highly concentrated markets, a handful of companies dominate the landscape, making it very difficult for new players to enter and potentially leading to anticompetitive behavior – like price fixing or collusion.

An unconcentrated market is typically very competitive, populated with many smaller players and no dominant force that would keep a new company from entering the space.

In the aircraft manufacturing business – a highly concentrated sector – just four companies capture 80% of the U.S. market.

By contrast, Colorado’s retail marijuana sector is highly unconcentrated, taking approximately 364 businesses to reach 80% of the market.

Adam Orens, a founding partner of Marijuana Policy Group, believes limitations on out-of-state ownership and investment in Colorado marijuana businesses, as well as legal uncertainty at the federal level, have kept the state’s nascent industry from further consolidation.

But Orens also believes that more investment – and more consolidation – in Colorado’s retail marijuana market is forthcoming amid signs that MJ reform efforts in Washington DC may be gathering momentum.

“More investment comes once you get stronger federal signals,” he said. “I’ve seen over the last year the types of investment, the types of capital coming into the market are getting more and more organized.”

And given how fragmented the market is now, Orens contends that – although not without some negative impacts – consolidation could bring about some positive developments for the consumer.

“What this consolidation does is it brings better products and services at better prices as the larger businesses compete,” he said. “Businesses would also be more compliant and have more professional operations, as they have more riding on it.”

Eli McVey can be reached at elim@mjbizdaily.com