(You can have cannabis finance content such as this delivered directly to your inbox. Simply sign up here for our weekly MJBizFinance newsletter.)

During the pandemic, interest in special purpose acquisition companies (SPAC) soared, as private cannabis-related businesses looked to these blank-check companies for quicker, easier access to public markets and the funding that comes with it.

But two years later, the sparkle seems to be dimming.

The ability to skirt some of the requirements for a standard initial public offering is drawing some unwanted attention for regulators.

And investors who were excited about the potential for a more modern way to access markets are facing the reality that maybe, just maybe, some of those rules really do have a purpose as the SPAC-origin companies underperform on that public market.

Matt Karnes, founder of New York-based Greenwave Advisors, told me that cannabis SPACs are more vulnerable to the negative sentiment around the overall market for a few reasons:

- SPACs can provide forward-looking statements and forecasts that other public companies must warn against. And the uncertainty that continues around cannabis legalization creates a lot of gray area around the quality of those statements.

- Cannabis companies have underperformed on those revenue forecasts – in large part because of continued market pressures from illicit operators.

- SPACs that successfully found targets have traditionally underperformed, but unlike mainstream industries, the cannabis space doesn’t have the same access to traditional sources of capital, so it’s more vulnerable to the swings.

But even with the diminished excitement around this funding channel, opportunity still exists.

“There is still $1 billion in SPAC capital hunting for companies in cannabis, with deadlines mostly in 2022-23,” said Mike Regan, founder of Denver-based MJResearchCo.

“Of this $1 billion, $491 million is looking for ancillary cannabis companies that don’t break any laws and $510 million targeting plant-touching operations.”

The key to succeeding on this path: Don’t overpromise and underdeliver.

It’s the same advice we’ve given for any company seeking funding in any manner.

Investors who once bought into the potential of cannabis are now seeing the reality. Gone are the days of pie-in-the-sky forecasts and valuations.

If you want to be a target for success, be realistic about where you expect to go.

And prepare for changes to where the industry currently is.

Subscribe to the MJBiz Factbook

Exclusive industry data and analysis to help you make informed business decisions and avoid costly missteps. All the facts, none of the hype.

What you will get:

- Monthly and quarterly updates, with new data & insights

- Financial forecasts + capital investment trends

- State-by-state guide to regulations, taxes & market opportunities

- Annual survey of cannabis businesses

- Consumer insights

- And more!

Deal of the Week / In partnership with Viridian Capital Advisors

U.S. cannabis consolidation 2.0

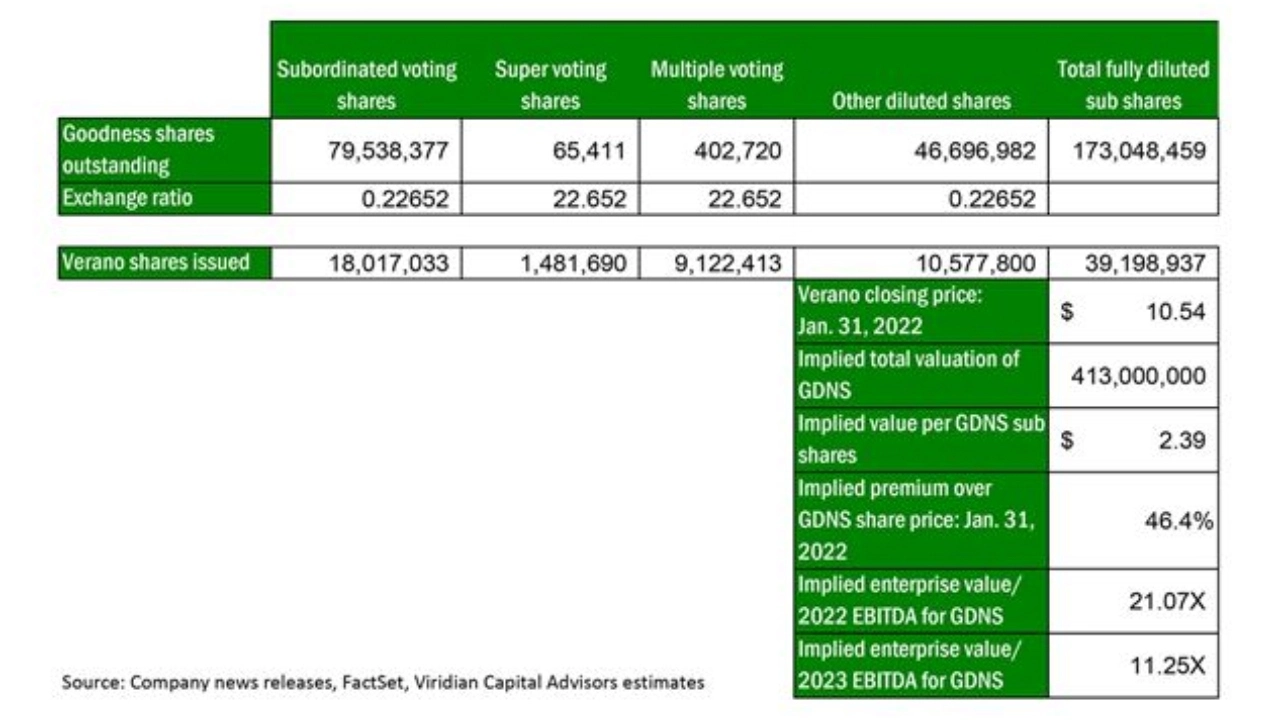

Verano Holdings (CSE: VRNO; OTCQX: VRNOF) agreed on Jan. 31 to acquire all outstanding shares of Goodness Growth Holdings (CSE: GDNS; OTCQX: GDNSF) in an all-stock transaction that values Goodness Growth at $413 million on a fully diluted basis.

The deal might be the first of many that abandons a common wisdom in cannabis M&A.

The acquisition ascribes a high valuation for Goodness Growth, based on 2022 and 2023 consensus EBITDA estimates.

- Verano is paying 21.07X Goodness Growth’s estimated 2022 EBITDA and 11.25X estimated 2023 EBITDA.

- The implied Goodness Growth share price of $2.39, based on the exchange ratio and Verano’s closing price on Jan. 31, is a 46% premium to GDNS’ closing price that day.

The deal is also 36% dilutive to Verano on a pro forma 2022 EBITDA per-share basis.

In conjunction with the transaction, Goodness Growth executed an amendment to its credit facility with Chicago Atlantic, allowing access to an additional $55 million of a delayed draw term loan for working capital, general corporate purposes and expansion of its New York operations.

Verano agreed to reimburse GDNS for all interest expenses above 10% until the closing or termination of the transaction.

The facility is relatively expensive, carrying a minimum cash interest rate of 13.375% and additional payment-in-kind interest of 2.75%.

The facility matures on April 30, 2023, and its refinancing represents an opportunity to improve the cash flow of GDNS.

The Viridian Credit Tracker ranks Verano as the fourth-strongest major multistate operator from a credit perspective, meaning it likely could refinance the debt at a rate below 9% after the deal closes.

Implications for the cannabis capital markets

Previously, Viridian Capital Advisors listed two potential catalysts that could make for a turnaround in cannabis stock prices:

- Significant new M&A activity.

- A renewed attempt at banking reform.

Both of these planks are now in place, and Tuesday’s stock prices show continued enthusiasm after a strong performance Monday.

Viridian has consistently pointed out that a significant driver of recent M&A activity is the gap between acquirer and target valuation multiples.

This transaction is the opposite: Verano is trading at only about 6.6X 2022 EBITDA, whereas the purchase price for GDNS implies a 21X multiple.

Verano is looking at the long-term strategic benefit of acquiring a portfolio of licensed and partially built-out assets that it can finish, improving its strategic and long-term financial position.

The New York license alone might be worth more than $200 million, and the opportunity to expand in this market justifies the premium valuation paid.

The market likely will see an uptick in strategic public/public M&A transactions, with the odds of more significant transactions increasing.

Other potential acquisition targets include Planet 13 Holdings and 4Front Ventures.

And larger, undervalued Tier 1 or 2 MSOs could begin to entertain strategic combinations.

Several of the top management groups of these companies come from investment banking backgrounds, and the financial and operating gains to scale are not lost on them.

The previous time cannabis stock prices fell off the cliff, it brought M&A activity to a virtual standstill.

This has not happened in the current market downturn, and this transaction represents why Viridian doesn’t expect it to.

The common wisdom is that since the stock is the primary acquisition currency, acquisitions should be less attractive when prices fall. The fallacy of this argument is twofold:

- Most acquisitions benefit from the valuation gap between large and small companies.

- That common wisdom looks at the transaction only from the buyer’s perspective.

Like many major MSOs, Verano stock has been heavily punished in the latter half of 2021 and early 2022, and 6.6X next year’s EBITDA represents an extraordinarily attractive investment.

Sellers increasingly appear to be looking at the long-term investment potential of the acquirer’s stock and prefer receiving discounted stock rather than cash.

GDNS might well be looking at Verano stock as the gift that keeps on giving.