(You can have cannabis finance content such as this delivered directly to your inbox. Simply sign up here for our weekly MJBizFinance newsletter.)

Deal of the Week / In partnership with Viridian Capital Advisors

Is Tilray’s investment in MedMen enough for either company to bloom in US markets?

Last week, British Columbia-based Tilray (TLRY on Nasdaq, TSX), the second-largest Canadian licensed producer by market cap, announced a transaction to gain a substantial interest in U.S. cannabis retailer MedMen.

Tilray and other strategic investors formed a special purpose vehicle (SPV) to acquire approximately 75% of the outstanding senior convertible notes and 65% of the facility warrants from Gotham Green Partners (GGP):

- The SPV will own roughly $165.8 million in principal on the notes and about 135.3 million warrants.

- The notes have a weighted average conversion price of 24 cents per share, and the warrants have a weighted average exercise price of 23.57 cents per share.

- Tilray has a 68% interest in the SPV, giving it an economic interest of $112.7 million via the notes and 92.0 million warrants. This provides Tilray an approximate 21% ownership in MedMen.

Using simple math, Viridian estimates that the total SPV would own about 30.9% of California-based MedMen.

In exchange for this contingent ownership position, Tilray agreed to issue roughly 9 million Tilray shares to GGP.

However, Tilray is running low on authorized shares, so the issuance requires shareholder approval. If approval isn’t given by Dec. 31, GGP has the right to receive cash.

Total consideration for the deal is $120.7 million (9 million shares at $13.41 per share), imputing a market cap of $574 million for MedMen.

The existing senior convertible notes will be modified by the deal:

- Maturity will be extended to Aug. 16, 2028.

- The minimum liquidity covenant will be removed.

- Interest will be payment in kind (PIK) with the PIK interest convertible (after the U.S. legalizes marijuana at the federal level) at market prices.

- The notes will be noncallable until after a legalization event, which would allow Tilray to convert its notes.

On Aug. 17, MedMen also agreed to sell approximately $100 million worth of units to Serruya Private Equity Group.

The deal consists of:

- 416.7 million units at 24 cents per unit.

- Each unit includes: one share and one-quarter warrant with an exercise price of 28.8 cents and a five-year life.

- Short-term warrants (one year) that allow investors to pay $30 million to acquire $30 million in convertible notes with a conversion price of 24 cents. Proceeds from the exercise of these warrants will pay down debt.

Viridian values the embedded options in this deal at a total of $8.7 million ($5.1 million for the unit warrants and $3.6 million for the short-term conversion options).

Net share price is 21.9 cents per share, a discount of 17.7% from the 26.6-cent share price on the day before the transaction.

This discount strikes us as reasonable given the circumstances of the sale.

While the stock market reacted positively, Viridian has a different view

Tilray is paying an excessive price for its investment in MedMen.

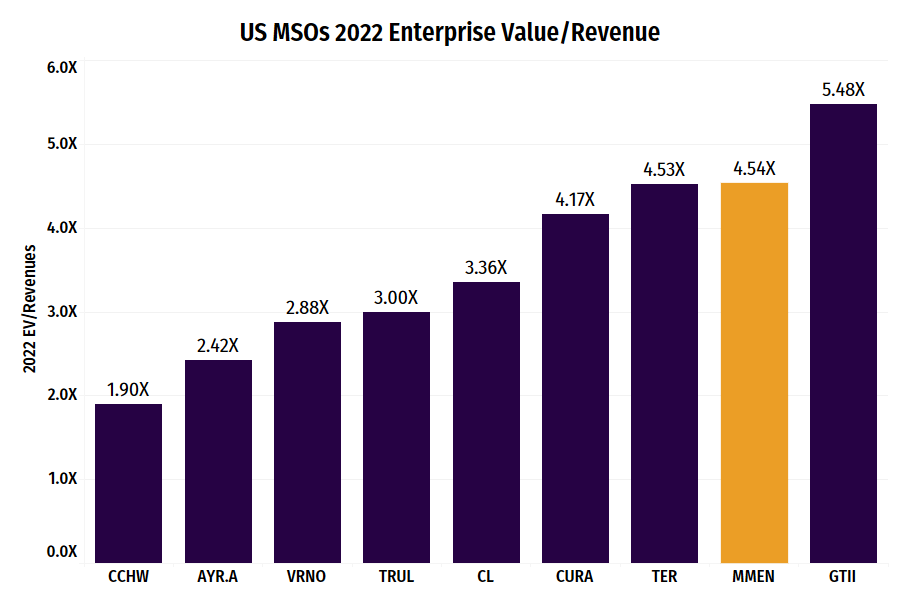

The implied enterprise value for MedMen is around $813 million (assuming conversion of all notes held by the SPV). Viridian Capital Advisors calculates an implied enterprise value/2022 consensus revenue of 4.54X.

Several comparable competitors have as good or better growth prospects than MedMen – and better profitability – so valuation near the top of the group is difficult to reconcile. Perhaps the optionality/safety of owning a debt instrument rather than straight equity is worth something, but not this much.

The $100 million infusion from Serruya is helpful, but will it provide enough liquidity to get MedMen to cash flow self-sufficiency?

MedMen’s cash flow from operations in its March quarter was -$14.7 million, and it has considerable CapEx requirements to complete its planned stores. Additional dilutive issuance would not be surprising.

This likely will be “dead money” for quite a while.

Viridian’s team does not believe the U.S. is on the cusp of federal legalization, and therefore this deal will represent a noncash-earning asset on Tilray’s books (albeit a relatively small one) for several years.

Despite progress by MedMen’s management in turning around the business, the company has lost its market leadership position and now is just another midsized MSO.

MedMen does have some excellent locations, including its soon-to-open store near Boston’s Fenway Park, but the company is not the market leader it once was perceived to be.

The acquisition will not get Tilray very far in its pursuit of $1.5 billion in U.S. revenue.

Consensus estimates have MedMen at less than $200 million for 2022. Furthermore, the strategy of quadrupling revenue through acquisitions is questionable. Viridian’s analysts DO understand Tilray’s desire to get into the U.S. market; its 8% consensus 2022 EBITDA margin tells you everything. CEO Irwin Simon clearly understands that Tilray cannot support its current market cap without massive revenue and profit increases – and MedMen might well be the only play that was available. It just doesn’t make a big enough difference to matter.

Consider Gotham Green’s motivation for this transaction.

There’s an old saying: If you can’t figure out who the chump at the poker table is, it’s you. Frankly, GGP is not the chump here.

- GGP stubbed its toe on MedMen, but its strategy has been quite clear for some time: Conserve optionality by maintaining a secured debt position while continually negotiating higher conversion positions in the company. Where necessary, GGP has been willing to provide extra liquidity to keep that optionality alive.

- Viridian’s analysts believe GGP was holding on, hoping that federal legalization would happen and a rich, dumb investor would pay up for the chance to take over MedMen. Some cracks in GGP’s certainty appeared with the sale of its New York assets in the face of an imminent adult-market conversion.

Along comes Tilray, willing to pay a hefty premium years ahead of legalization. And we imagine that GGP would not mind taking the cash instead of the 9 million Tilray shares.