Former Nova Scotia Premier Darrell Dexter is calling on the federal government to address banking issues stymieing legal marijuana businesses across Canada.

Almost one year into adult-use legalization, cannabis entrepreneurs and registered not-for-profit trade associations are accusing Canada’s banking sector of gouging and arbitrarily closing bank accounts – sometimes citing U.S. federal law that prohibits marijuana.

Banks contacted for this story said they review each application on a case-by-case basis or declined to comment.

The lack of access to banking services is creating a litany of problems for cannabis enterprises, raising barriers to entry for prospective businesses, including:

- Paying bills.

- Payroll challenges.

- Aquiring credit.

- Complicating M&A transactions.

- Making it nearly impossible to pay the federal payroll tax – lest Revenue Canada start accepting bags of cash.

The main banks’ cannabis policies are frustrating regulated businesses. On the one hand, the banks are opening up to large producers by offering loans, but, on the other hand, smaller businesses say they face arbitrary and inconsistent hurdles.

“It’s confounding,” said Dexter, who is vice chair of Global Public Affairs and head of the Cannabis Beverage Producers Alliance (CBPA), an industry group representing marijuana drink businesses.

“Here we are, almost a year into recreational legalization. Medical cannabis in the regulated market has been there for many years, and yet people are still having difficulties getting their banking requirements.

“How do you carry out transactions if you’re a company in the legitimate space if you don’t have banking? That is a huge barrier to entry into what is a legal, regulated market.”

The CBPA, a registered not-for-profit trade association, saw its account shuttered.

“It’s very hard to understand how we can be having these types of issues a year into it.

“We’re not the exception,” he said.

Dexter wants to meet with the minister of finance after the Oct. 21 federal election to discuss potential solutions.

“The Department of Finance regulates the banking sector. What is the issue the banks think they are fixing by not allowing companies in the legitimate cannabis space (to have their) banking requirements met?” he asked.

‘Shameful’

Thomas Clarke, founder of the licensed retailer THC Distribution in Newfoundland, was turned away in his attempts to open an account with Canadian Imperial Bank of Commerce, TD Canada Trust and Scotiabank.

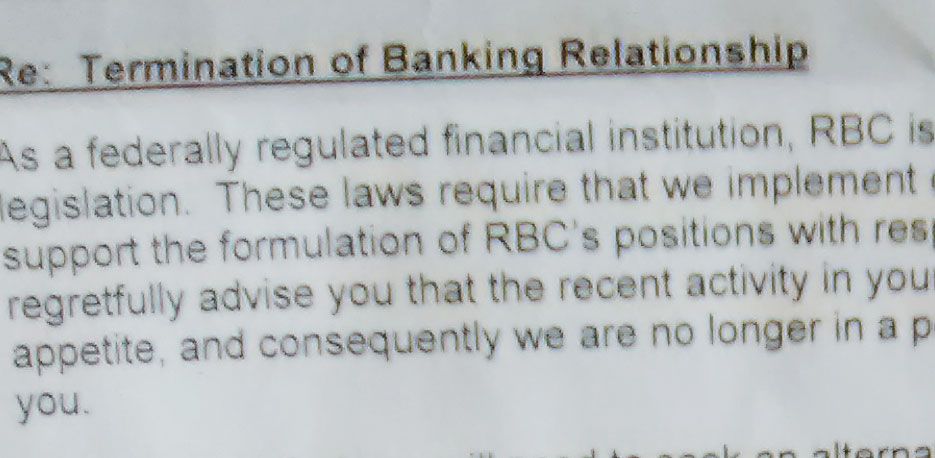

That was after Royal Bank of Canada closed his account.

The Bank of Montreal (BMO) even asked Clarke for a nonrefundable payment of 7,000 Canadian dollars ($5,300) for the privilege of applying to open a bank account.

Clarke said he wasn’t prepared to write a check for CA$7,000.

“I can’t throw away CA$7,000 like that,” he said.

The next day the bank “flat out” denied him.

It’s not an isolated case. The same bank forced current and prospective clients in Ontario to pay CA$3,000 for an “initial review” of operations and documents, according to documents viewed by Marijuana Business Daily. It also imposed an annual charge of CA$1,000 for “monitoring and maintenance.”

Tax was not included, and no service was guaranteed, meaning BMO could arbitrarily reject clients – as it did Clarke – with no chance of refund.

Clark said he was told – in person – he was being rejected because of U.S. federal law.

Clarke said he was told by four of the five banks that “we do business in America, and because our American counterparts don’t want us doing business with cannabis businesses, we are not taking on any clients at this time.”

Like so many others in the cannabis sector, Clarke is turning to Ontario-based Alterna Bank – but the closest branch is more than 1,500 kilometers (932 miles) away.

“I think that’s ludicrous. As a small-business owner of a mom-and-pop shop,” Clarke said, “I can’t believe that America and the cannabis stigma are playing a role in small-town Canada’s cannabis operations.

“That’s what’s happening, according to the banks themselves. This is shameful.”

‘Unable to bank’

Lisa Campbell’s Lifford Cannabis Solutions in Toronto is one of the companies operating within the boundaries of the regulated cannabis industry that remains unable to get normal business banking services – nearly a year after marijuana was legalized.

After recently applying for a business and trading account with TD Canada Trust, the account was opened before being immediately frozen, she said.

Lifford – also co-chair of Cannabis Beverage Producers Alliance – was unable to use the accounts nor deposit shares from a recent deal.

“I don’t have a business line of credit,” she said. “All I’m able to secure for my company right now is a checking account. I don’t have normal banking services that all other businesses have access to. Even though I’m generating a lot of revenue, I’m not able to have normal banking services.”

“How do you focus on your business when you’re trying to get a bank account all the time? We spend so much time dealing with banks. They should be happy to take our money.”

Banks respond

MJBizDaily reached out to Canada’s five largest banks to seek clarity on their cannabis business banking policies. None answered the questions provided.

Following are their responses in full:

- CIBC: “We support emerging Canadian industries. For the cannabis sector, we review opportunities on a case-by-case basis.”

- Scotiabank: “We don’t have a comment for your story.”

- RBC: “RBC evaluates banking relationships within the sector on a case-by-case basis. Decisions are made against a number of factors, including: the nature of their business, their financial position, creditworthiness, their ability to comply with legal and regulatory requirements, as well as other factors relevant to their specific business. This issue has many dimensions, and the law and regulatory framework for the sector continue to evolve. We will continue to take all factors into account within the context of our banking policies. Beyond that, we do not comment on our banking relationships.”

- BMO and TD did not respond.

If you’re the proprietor of a cannabis business who is willing to share an experience with one of these financial institutions, email Matt Lamers at mattl@mjbizdaily.com