A second round of multistate marijuana operators are rapidly expanding their geographic footprints, taking advantage of acquisition and licensing opportunities as well as their ability to raise financing.

The companies appear to be trying to follow in the footsteps of established MSOs such as Massachusetts-based Curaleaf, Illinois-based Green Thumb Industries and Illinois-based Cresco Labs.

The upstart MSOs show signs of being “up-and-comers,” but experts caution that what might look good in news releases must still be proved on the ground.

“But the value that needs to be proven to investors and customers is their ability to operate profitably – beyond their ability to raise capital.

“There’s too much emphasis on the ability to raise money as a proxy to managing a company well.”

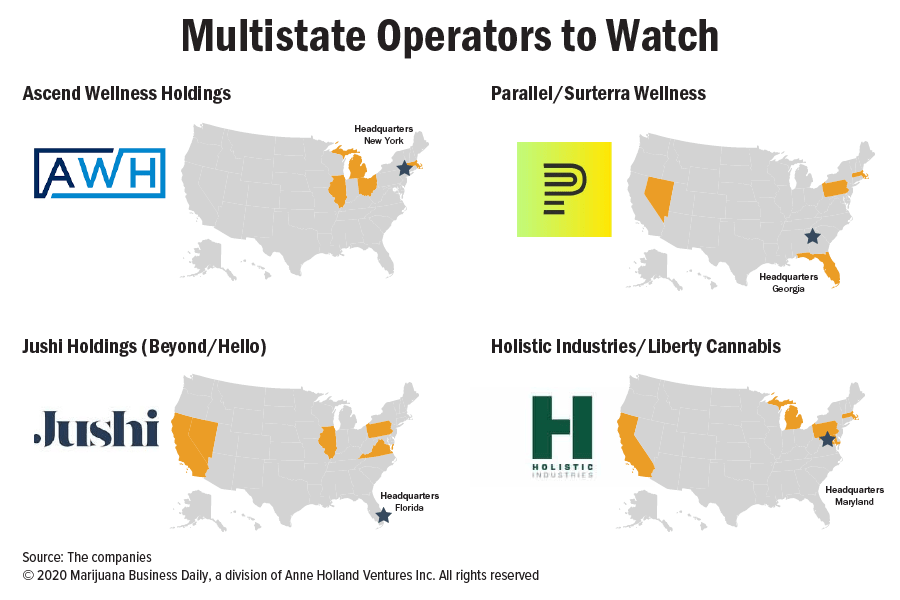

Marijuana Business Daily identified four MSOs to watch in the next year (see each company and its footprint in the graphic above), but many others are expanding operations in multiple markets as well.

The four – New York-based Ascend Wellness Holdings (AWH), Maryland-based Holistic Industries, Florida-based Jushi Holdings and Atlanta-based Parallel – have a few factors in common:

- Strong financial backing or the ability to secure funding via capital markets that are beginning to loosen up.

- An expanding footprint in new or existing markets through build-outs or targeted acquisitions.

- A strategy focused on markets that have high-growth potential and limit the number of available licenses.

AWH, Jushi and Holistic recently have raised capital:

- AWH in August closed on a $68.2 million funding round mostly for expansion. It recently acquired two marijuana retailers in Chicago from Modern Cannabis, giving Ascend six in the state.

- Jushi raised $33.3 million in debt financing in late July and, less than two weeks later, closed on a $37 million deal to acquire Vireo Health’s cultivation and processing operation in Pennsylvania. The move enables Jushi to meet product demand in the state’s fast-growing medical cannabis market and position itself for a likely adult-use market in the near future. The company brands its retail outlets as Beyond/Hello.

- Holistic said Tuesday it closed on a $35 million debt financing that will be used to complete cultivation and processing build-outs and pursue additional licensing and distressed-asset opportunities. “This will be the only debt on the company’s balance sheet,” Holistic said in a news release. The company’s flagship retail and wholesale brand is Liberty Cannabis.

The fourth MSO highlighted – Parallel – is headed by William “Beau” Wrigley, a former CEO of the Wrigley’s chewing gum empire. Forbes magazine recently listed Wrigley’s net worth at $3.1 billion.

Parallel changed its corporate name from Surterra Wellness in 2019 but still uses the Surterra brand in Florida.

Have strategies changed?

Livingston said this group of MSOs by and large have strategies that are similar to those of the first phase of MSOs, which were able to tap capital markets and expand their footprints rapidly in 2018 and 2019.

“I’m skeptical of anyone talking about a secret sauce,” Livingston said.

Several of those first-phase MSOs continue to do well, but others have run into cash crunches and have had to cut costs, sell assets and scrap acquisitions.

So it’s too early to know how this wave of MSOs will do, especially since most are privately held and critical metrics such as operating expenses and product profit margins are kept out of public view. Of the four, only Jushi is publicly held.

The reality is that the private MSOs are unable to go public as easily as their predecessors.

Many investors have soured on the cannabis industry because of the failure of operators to show profits, industry experts say.

What is the true intent of these MSOs?

Lee Dorkin, founder of Colorado-based Emprouen Advisors, a cannabis management and consulting firm, said he is still seeing too many MSOs with a strategy based on how quickly they can expand their geographic footprints, acquire assets and exit at a profit.

“That’s putting the cart before the horse,” said Dorkin, former head of U.S. operations for Origin House, a Canadian-based cannabis company that Cresco Labs acquired earlier this year.

“It’s a compression of the realistic time needed (to perform) due diligence, acquire and integrate companies, streamline operations, stabilize leadership, and benefit from the roll-up (of assets).”

He cited one MSO that already was planning an exit strategy through acquisition in multiple states and then a public stock offering – without having done enough due diligence to realize it didn’t meet state vertical regulatory requirements to complete the acquisition.

Not knowing the jurisdictional requirements can be very costly, Dorkin said.

Dorkin also said the strategy of going after limited-licensing markets might be a fallacy, especially during a COVID-19 environment in which states and local jurisdictions are under increasing pressure to raise tax revenues to cover budget shortfalls.

“I think you’re going to find an acceleration of licensing being approved in states,” he said. “The licensing assumptions of today might be a completely different reality tomorrow.”

What does that do to a company that has based its model on a limited-license scheme? “When the number of licenses allowed in a market substantially increases, the value of existing licenses are diluted or decline,” he noted.

Dorkin said the smart MSOs ask themselves hard questions about the purpose of their multistate business structure and why they are entering particular markets.

“For top-line or revenue growth? Because they are missing parts of their vertical operation such as manufacturing, distribution, retail or cultivation? To acquire brands? To acquire intellectual property? For multiple arbitrage (simultaneously buying and selling assets)? For value creation?”

Experts said MSOs also must weigh what is economically advantageous in anticipation of a changing regulatory landscape and eventual federal reform.

Livingston noted that MSOs that develop vertically integrated operations in each of their markets don’t enjoy the same economies of scale as do traditional industries because “they can’t transfer product across state lines because of the federal prohibition on cannabis.”

It’s also difficult to tell how well marijuana businesses are doing because most states don’t divulge companies’ sales figures.

Florida is an exception, which provides weekly sales data by operator.

For example, Parallel, doing business as Surterra Wellness in Florida, operated 39 dispensaries in the state as of Sept. 10, second only to Trulieve and a number equal to nearly 15% of the state’s 274 dispensaries.

Yet Surterra had only about a 10% market share of sales, according to the Florida health department’s weekly update for Sept 3-10.

But the company presumably has deep pockets thanks to Wrigley and operations in adult-use markets such as Massachusetts.

Parallel also recently signed a research partnership with the University of Pittsburgh. The deal provides Parallel entry into the strong Pennsylvania MMJ market through the right to open six dispensaries and, like Jushi, position itself for possible adult-use legalization.

But time will tell how well Parallel and these other MSOs do and which, as Livingston said, are good at raising money “but not all that good at managing and operating.”

Jeff Smith can be reached at jeffs@mjbizdaily.com