(Editor’s note: Codie Sanchez of Entourage Effect Capital is writing the first in a recurring series of commentaries from professionals connected to the cannabis industry.)

(Editor’s note: Codie Sanchez of Entourage Effect Capital is writing the first in a recurring series of commentaries from professionals connected to the cannabis industry.)

As we are sure you have noticed, the market in cannabis is strained.

Gone are the days of raising on multiples of forward-looking earnings and limitless capital inflows. The easy days in capital raising are, for the time being, behind us.

In a few short months, the cannabis market has moved from a license-aggregation phase, to a product innovation phase, to a market share-grabbing phase, to – finally – a true execution phase.

All of this will be good for the industry in the long term, but there comes a short-term, and bloody, price. That price is this correction.

What is happening

Generally, when the stock market corrects, it bounces back. But every so often, there is contagion, and it impacts everyone. Today it is contagion in cannabis.

The contagion in the cannabis sector has been driven by easy Canadian licensed producer money turning off premature IPOs, missed expectations on earnings and an infusion of retail money at very aggressive valuations – which no longer represent current conditions.

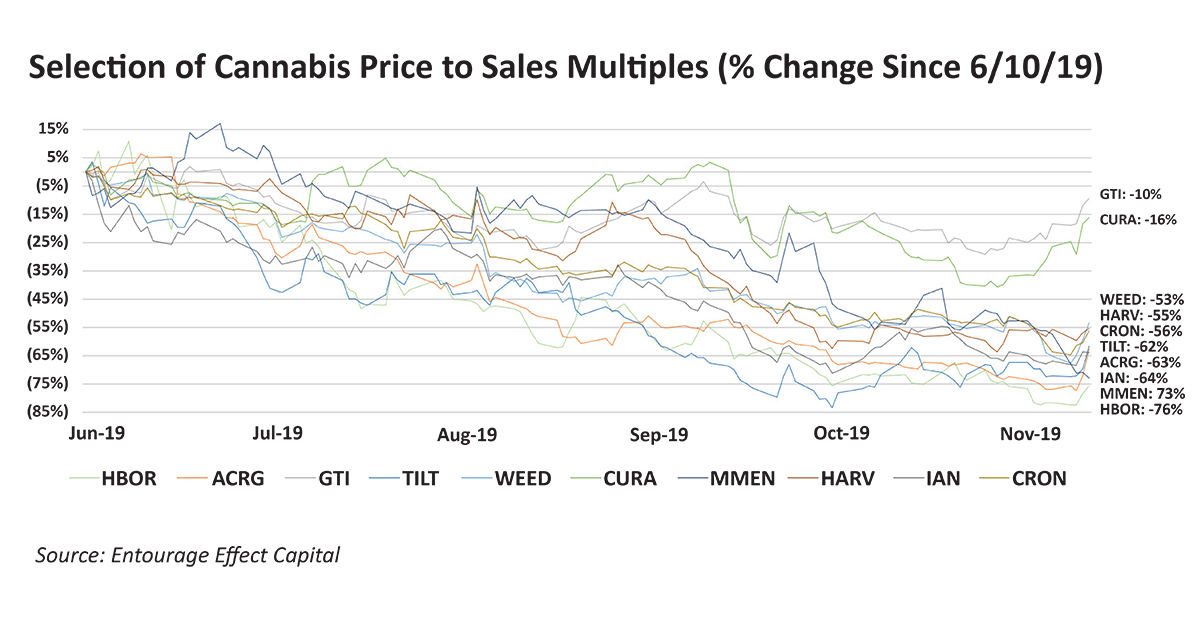

Regardless of the reason, the image below is what is happening in cannabis today in the public markets. Across the board. Companies are in the red – down anywhere from 20% to 80% – and we have not seen the bottom.

Given the fact that these same companies were the largest industry acquirers, it’s safe to say they will no longer be making a slew of high-valuation acquisitions to save the day in the short term.

We have seen this come to fruition as M&A deals in cannabis were cut in half this quarter, zero all-cash deals happened and earnings were missed by 30% of companies on average, according to Viridian Capital.

The downturn is real.

Here’s the truth of what happens after an “event” such as this:

- Stocks sell off aggressively.

- The selloff continues with false bottoms and finally bottoms out (usually after two to five quarters).

- During this period, no one is really doing anything. Fear paralyzes investors.

- Those who get the easiest funding (or any funding) during this period are proven winners that might not even need it. However, the strategic ones will take the funding to further capitalize on the market’s buying opportunities.

- Profitable companies might also get funding – but at haircut pricing with down rounds, warrants and liquidation preferences attached.

- Companies that are not profitable, or have a short runway and high cash burn, will struggle to get funding.

- Brand-new ventures will find the markets difficult, if not impossible, to raise in and they’ll get a significant discount on price.

The silver lining:

Well-capitalized companies stand out because as stocks fall, so do costs. Thus, the company’s Advertising Cost of Sales (ACoS) falls, talent costs fall, services come in at 50% the cost and M&A costs fall.

This is where those who are strategic now start to shine.

Markets always regress to the mean or become profitable again at some point. The only question is which cannabis companies are prepared to weather the storm in the meantime?

What cannabis companies need in 2020

Cannabis company founders and CEOs need to know the following as 2020 begins:

- Do they have a 12- to 18-month runway?

- Do they have a real handle on their finances and cash management?

- Are they (or can they get to) profitability with the money they have?

- Are they a top-performing company in the space (the top 25%)?

The four ways cannabis companies will act in 2020:

- Calling for help: Look for several companies to seek out private equity to, at best, facilitate mergers and, at worst, avoid bankruptcy. For the past few years, private equity firms have been building war chests waiting for this period of reckoning.

- Focusing on sales: Look for companies to make every effort to be more efficient, preserving margins while aggressively seeking out new customer bases.

- Containing cash: Exploratory innovation will take a back seat to very little beyond essential capital spends. Profitability will matter.

- Merger mania: Oftentimes, companies are stronger together. PayPal merged with X.com when they were competing. Dell and EMC Corp.; Anheuser-Busch InBev and SABMiller – they merged as there were internal issues apart. A powerful merger can weather a storm.

Codie Sanchez is managing director of Entourage Effect Capital. She can be reached at csanchez@eecpartners.com.

For analysis and in-depth looks at the investment trends and deals driving the cannabis industry forward, sign up for our premium subscription service, Investor Intelligence.

To be considered for publication as a guest columnist, please submit your request here by filling out our form.