The stocks of U.S.-focused operators have rallied while Canada-focused operators have underperformed in the second-quarter earnings season, closing the valuation gap on enterprise value-to-2021 sales.

The rally in the United States bodes well for the thawing of the capital markets for U.S. operators – at least for those that can show strong and profitable revenue growth.

Since at least January and as recently as April, U.S.-focused stocks have traded at a discount to Canada-focused stocks, despite showing faster revenue growth and higher margins in a larger market with more legalization catalysts.

Federal illegality in the U.S. subjects the operating companies to an onerous tax rate under IRS Section 280E, limits their access to traditional banking and prevents investment by many institutional investors and traditional consumer-operating companies.

Mike Regan

If nothing changes, Canada arguably should trade at a higher valuation because marijuana is federally legal there and cannabis firms pay a normal tax rate.

But if you expect legalization to expand in the United States, then the resolution of these issues is precisely the reason for higher multiples for the U.S.-focused operators.

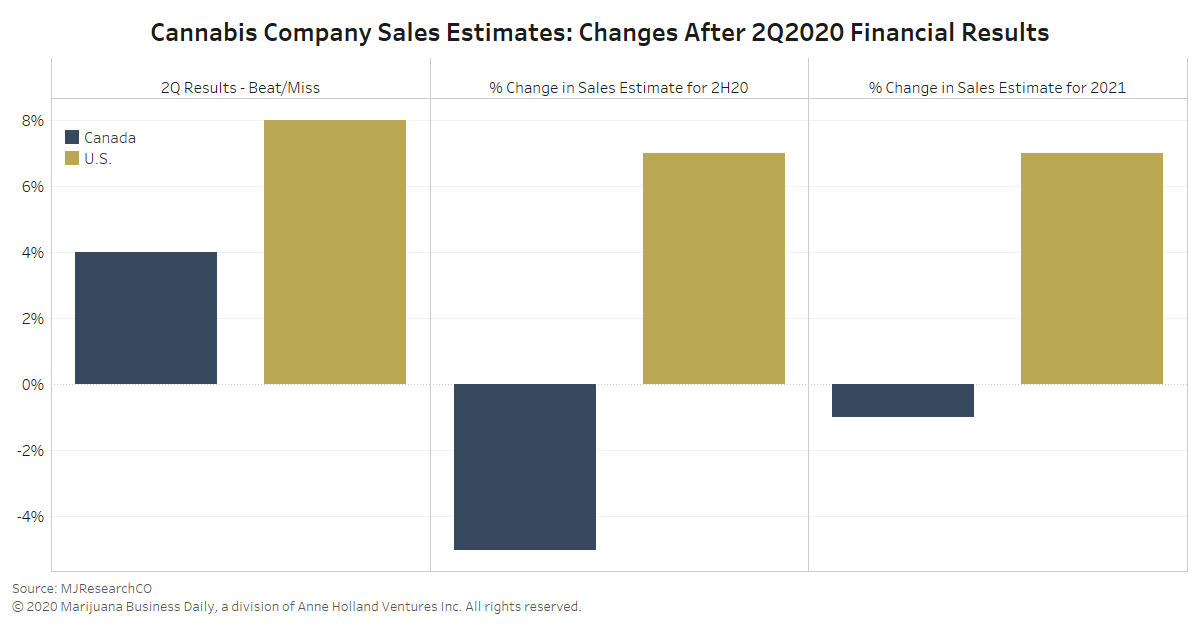

Increasing US growth vs. estimate cuts in Canada

The general theme for second-quarter earnings for the U.S.-focused operators was resiliency and stronger-than-expected sales results during the COVID-19 pandemic, while Canada-focused firms discussed price pressure and capacity rightsizing.

As shown in the chart below of larger public cannabis stocks that reported second-quarter earnings in July and August, the U.S.-focused public stocks have increased an average of 15% since reporting while the Canada-focused public stocks have dropped an average of 8%.

The second-quarter sales results were generally in line or beats for the U.S., while nearly half those reporting in Canada missed expectations.

Since valuations and stock prices are always forward-looking, the more important driver for the stock prices is the change in forward estimates.

The Canadian sales estimates for the second half of 2020 declined 5% on average; for 2021, those estimates declined 1%.

By contrast, the forward estimates for the U.S. stocks increased 7%. Excluding the massive beat and raise at supplier GrowGeneration and Curaleaf’s increase stemming from the inclusion of Grassroots Cannabis, forward estimates still increased 3%.

| Ticker | Name | 2Q20 Report Date | Return 2Q Report to 8/17/2020 | 2Q20 Beat /Miss | 2H20 Sales Estimate Change | 2021 Sales Estimate Change |

| VGWCF | Valens Co. | July 15 | 18% | -9% | -33% | -15% |

| CGC | Canopy Growth Corp. | Aug. 10 | 2% | 15% | 1% | -1% |

| OGI | Organigram Holdings | July 21 | -5% | -16% | -21% | -15% |

| TLRY | Tilray | Aug. 10 | -5% | -8% | -7% | -9% |

| TGODF | The Green Organic Dutchman Holdings | Aug. 13 | -8% | -3% | 0% | 6% |

| LABS | MediPharm Labs Corp. | Aug. 13 | -13% | 31% | 3% | 0% |

| VFF | Village Farms International | Aug. 12 | -20% | 15% | 17% | 7% |

| CRON | Cronos Group | Aug. 6 | -20% | 7% | -6% | -7% |

| APHA | Aphria | July 29 | -25% | 2% | 1% | 20% |

| Canada-Focused Average | -8% | 4% | -5% | -1% | ||

| GRWG | GrowGeneration Corp. | Aug. 13 | 84% | 19% | 24% | 24% |

| FFNTF | 4Front Ventures Corp. | July 14 | 40% | 8% | 0% | -3% |

| TCNNF | Trulieve Cannabis Corp. | Aug. 12 | 15% | 14% | 17% | 12% |

| IIPR | Innovative Industrial Properties | Aug. 5 | 14% | 1% | 2% | 6% |

| CCHWF | Columbia Care | Aug. 10 | 13% | -4% | -14% | 0% |

| GTBIF | Green Thumb Industries | Aug. 12 | 9% | 16% | 12% | 8% |

| CURLF | Curaleaf Holdings | Aug. 17 | 5% | 6% | 19% | 24% |

| ACRGF | Acreage Holdings | Aug. 14 | -5% | 0% | 2% | 3% |

| HRVSF | Harvest Health & Recreation | Aug. 11 | -9% | 14% | 6% | 2% |

| GNLN | Greenlane Holdings | Aug. 7 | -16% | 10% | 0% | -3% |

| US-Focused Average | 15% | 8% | 7% | 7% | ||

| Courtesy of MJResearchCo | ||||||

On conference calls to discuss the results, executives at U.S. companies typically noted that cannabis sales acted more like resilient consumer staple products in the face of COVID.

“We are seeing increased demand across the country without exception,” said Joe Lusardi, CEO of Massachusetts-headquartered Curaleaf.

Kim Rivers, CEO of Florida-based Trulieve, noted that “patient behavior continued trending toward previous norms.”

By contrast, the Canadian market noted price pressure as the market shifted to value brands to gain share from the illicit market.

While cutting price to drive volume is a logical strategy for an oversupplied market, investors are typically wary of price cuts to drive volume given the potential impact to margins if costs cannot be similarly cut.

Canopy Growth CEO David Klein admitted as much on the Ontario, Canada, company’s second-quarter conference call.

“I know some are concerned about the growth of the value segment and potential for further price compression in the industry. … (The) value segment plays an important role in converting illicit sales into legal sales,” he said.

Klein later noted that “our ability to compete in all price segments will help build scale, which will enhance our margins.”

Ontario-based Aphria also noted price pressure from a shift to value product. Despite having nearly 500 million Canadian dollars ($380 million) on the balance sheet, the company announced a $100 million at-the-money offering.

Valuations now in line, but US cheaper on EBITDA

With the rise in the U.S. stocks and the decline in the Canadian companies’, the past Canadian premium has now vanished. The two segments now trade at similar valuations on sales, while the U.S. still trades at a discount on EBITDA.

As shown in the chart below, the U.S.-focused stocks that have reported trade at an average of 3.5 times sales estimates for 2021, while the Canada-focused stocks now trade at an average of 3.2 times sales estimates for 2021.

The valuations are starting to incorporate continued price pressure in Canada and the strong margins and improving regulatory outlook in the U.S.

Though average revenue growth is similar for the two, the U.S. is expected to show much higher EBITDA profitability with an average margin of 28% (22% excluding Innovative Industrial Properties’ 88% margin) vs. break-even on average for Canada.

This leads to a lower valuation at 15.0 times 2021 EBITDA for the U.S.-focused companies vs. 29.5 times for the Canada-focused operators.

| Ticker | Name | Enterprise Value / 2021E Sales | Enterprise Value / 2021E EBITDA | Sales Growth Estimate 2021 | EBITDA Margin Estimate 2021 | Return QTD 6/30-8/17/2020 |

| VGWCF | Valens Co. | 1.6 | 6.2 | 58% | 26% | 2% |

| CGC | Canopy Growth Corp. | 10.6 | n.m. | 45% | -24% | 5% |

| OGI | Organigram Holdings | 2.5 | 15.3 | 36% | 16% | -7% |

| TLRY | Tilray | 3.5 | 122.1 | 49% | 3% | -1% |

| TGODF | The Green Organic Dutchman Holdings | 2.8 | n.m. | 115% | -2% | 14% |

| LABS | MediPharm Labs Corp. | 1.0 | 5.3 | 86% | 18% | -23% |

| VFF | Village Farms International | 1.5 | 12.1 | 14% | 13% | 7% |

| CRON | Cronos Group | 3.3 | n.m. | 128% | -60% | -7% |

| APHA | Aphria | 2.2 | 16.1 | 23% | 14% | 4% |

| Canada-Focused Average | 3.2 | 29.5 | 62% | 0% | -1% | |

| GRWG | GrowGeneration Corp. | 2.7 | 25.7 | 46% | 11% | 136% |

| FFNTF | 4Front Ventures Corp. | 2.2 | 9.1 | 88% | 24% | 67% |

| TCNNF | Trulieve Cannabis Corp. | 4.1 | 9.4 | 32% | 44% | 88% |

| IIPR | Innovative Industrial Properties | 8.9 | 10.1 | 73% | 88% | 38% |

| CCHWF | Columbia Care | 2.2 | 11.7 | 119% | 19% | 44% |

| GTBIF | Green Thumb Industries | 4.7 | 14.5 | 48% | 33% | 58% |

| CURLF | Curaleaf Holdings | 6.0 | 18.0 | 88% | 33% | 55% |

| ACRGF | Acreage Holdings | 1.0 | 9.7 | 54% | 10% | 18% |

| HRVSF | Harvest Health & Recreation | 2.4 | 12.6 | 53% | 19% | 47% |

| GNLN | Greenlane Holdings | 0.5 | 29.1 | 22% | 2% | -25% |

| US-Focused Average | 3.5 | 15.0 | 62% | 28% | 53% | |

| Courtesy of MJResearchCo | ||||||

A thaw in US capital markets?

For private marijuana companies, the rally in U.S.-focused stocks might be the first step to thaw the frozen private capital markets – at least for private companies that can clearly communicate a quick path to positive cash flow (if not already generating it) and simple capital structures.

These tables skew to such qualities because they list only the companies of scale that reported during the second-quarter earnings season before Aug. 18.

Consequently, the tables do not include companies such as MedMen Enterprises and iAnthus Capital Holdings, which are in the process of restructuring their capital structures, or smaller companies with market capitalizations below $90 million.

Others companies, including Ayr Strategies, Cresco Labs, Planet 13, TerrAscend and Vireo Health International, are expected to report their second calendar quarters in the next week.

Mike Regan is the founder of MJResearchCo and a regular contributor to Marijuana Business Daily. He can be reached through his LinkedIn page or at info@mjresearchco.com.

Earnings details from some publicly traded companies in the cannabis industry are available here.