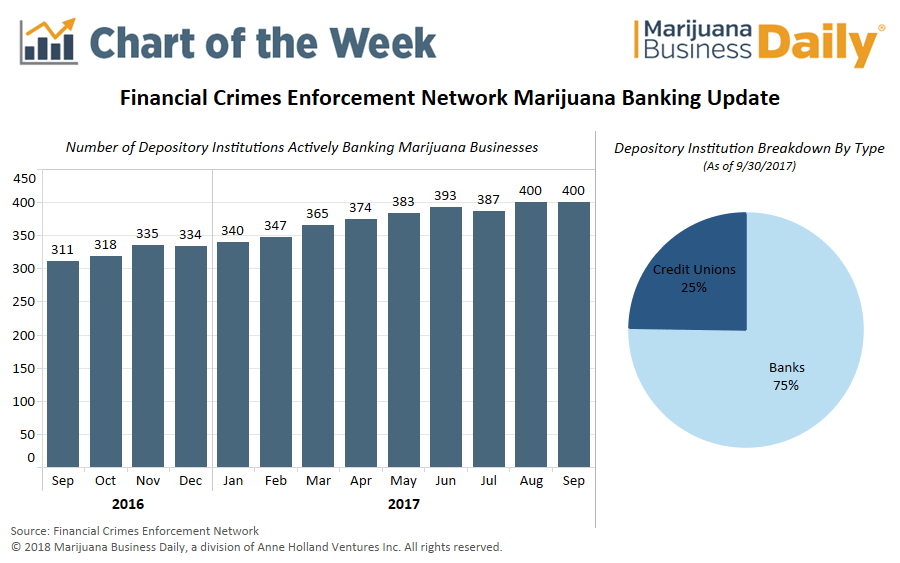

The number of banks and credit unions actively serving the marijuana industry has jumped nearly 30% from a year ago.

But U.S. Attorney General Jeff Sessions’ decision to repeal the Cole Memo may prevent further involvement by banking institutions looking to work with cannabis-related businesses.

Guidance outlined in a February 2014 FinCEN memo spurred the increased access to banking services, as it provided banks with a much-needed framework for how to work with clients in the marijuana industry.

Generally speaking, the memo requires financial institutions to verify that marijuana companies are properly licensed by the state and to monitor any financial wrongdoing and report suspicious activity to regulators.

Although Sessions ripped up the Obama-era Cole Memo protections, banks and credit unions serving clients in the marijuana industry were not immediately affected by this decision – as the guidance outlined in the February 2014 FinCEN memo is completely separate from the Cole Memo.

However, the scrapping of the Cole Memo – combined with a top Treasury Department officials’ statement that the Trump administration is reviewing the FinCEN safeguards – has further muddied the water in a situation that was unclear to begin with.

Marijuana remains illegal under federal law and the risk – no matter how small – of losing a federal license or incurring some other punishment has proved too much for most financial service providers to stomach.

Here’s what you need to know:

- Combined, there are over 11,000 banks and credit unions operating throughout the United States, meaning less than 4% of U.S.-based financial institutions are serving marijuana businesses. Many banks that do provide services to cannabis companies prefer to keep quiet about it, however, making it especially difficult for marijuana businesses to find a financial services provider.

- Financial institutions that knowingly provide banking services to cannabis businesses often charge a premium for their services. A marijuana business in Maryland recently reported paying monthly fees in excess of $1,700 to use a local bank.

- Banks account for the vast majority of financial institutions that serve cannabis businesses, with credit unions making up just a 25% share – as shown in the pie chart. This suggests that larger institutions have the resources needed to cater to the marijuana industry, given the regulatory hurdles involved with serving a sector that’s illegal under federal law. In fact, less than 30% of U.S. credit unions manage more than $100 million in assets, according to a report from the Credit Union National Association.

Eli McVey can be reached at elim@mjbizdaily.com