The number of banks and credit unions providing services to marijuana businesses has grown dramatically over the past 24 months, providing some much-needed relief to the cannabis industry.

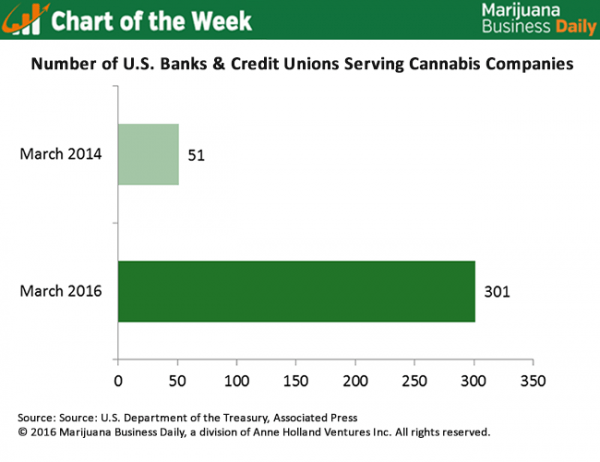

In March of this year, 301 financial institutions were working with marijuana companies, according to federal data obtained by the Associated Press.

That’s up from just 51 in March 2014 and a three-fold increase from later that year, when an estimated 100 banks and credit unions worked with the industry.

The increased access to banking services is no doubt an immensely positive development for the industry.

But cannabis companies still face many challenges on this end.

Nevertheless, the latest figures show that a growing number of banks are becoming comfortable with the notion of providing services to marijuana businesses.

Part of that is likely tied to guidance the U.S. Treasury Department’s Financial Crimes Enforcement Network issued in early 2014 that lays out steps financial institutions must follow to serve marijuana businesses in states that have legalized medical or recreational cannabis.

That said, just about all of those banks that have marijuana related clients prefer to keep mum about their accounts, lest they invite unwanted scrutiny from federal regulators.

Mum or not, it is in banks’ best interests to start serving the cannabis industry, said Patrick Moen, a former DEA agent and current general counsel at Privateer Holdings, a Seattle-based private equity firm that owns marijuana businesses.

In fact, Moen said many financial institutions probably already are serving the industry in some way or another, whether they know it or not.

“The greater risk to banks is to deny accounts to marijuana businesses and force them to employ subterfuge to get or maintain an account,” said Moen. “It’s much safer for a bank to say, yeah, we’re going to bank this industry.”

Omar Sacribey can be reached at Omars@mjbizdaily.com