By Becky Olson

Roughly 60% of companies operating in the cannabis industry don’t have bank accounts for their businesses, according to first-of-its-kind data from a survey conducted by Marijuana Business Daily.

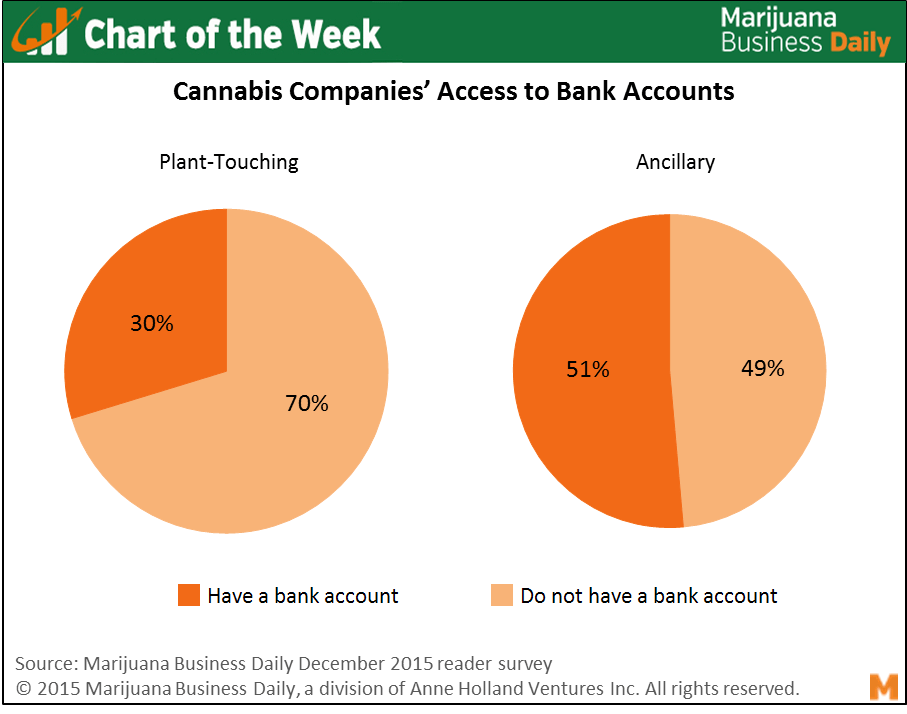

The situation is even worse for companies that actually handle the plant, with 70% reporting that they’re currently operating without traditional banking services.

The poll, which includes the responses of over 400 cannabis professionals from across the country, also found that a surprising 49% of ancillary firms don’t have bank accounts. This underscores how difficult the situation is even for companies that don’t touch marijuana, such as consultancies, software providers and other firms that sell products and services to the industry or cannabis consumers.

While the industry’s banking problems are well known, there has been little data or research on the issue of how many companies are operating with banking relationships.

Among the plant-touching industry sectors, wholesale cultivation companies have the lowest rate of access to the financial system – 81% of these businesses don’t currently have basic services such as a checking account. The circumstances for infused products makers and MMJ dispensary/rec store retailers are somewhat rosier by comparison, but 68% and 54% of those businesses, respectively, nevertheless still don’t have bank accounts.

Nearly 30% of companies without a bank account report they are actively seeking one, and another 13% are not currently pursuing one but have tried to in the past.

“Over the past six years I have had 14 accounts closed for the business,” said Tim Cullen, CEO of Colorado Harvest Company, which operates several cannabis retail shops and grows and currently has a business checking account.

Cullen went on to say that the process of obtaining the company’s current account was more time consuming and difficult than getting local and state licenses to operate the business.

“[Anything] and everything that the business has done in a financial sense as well as detailed personal history of the owners and their spouses” was required to get a bank account, he said.

However, a checking account still doesn’t allow a business to process card payments or finance equipment or real estate, posing major ongoing challenges to daily operations and strategic growth.

Finally, even if cannabis professionals are able to eventually secure any/all banking services for their businesses, they still face the prospect of having personal accounts closed.

“Just this past month a bank….closed my personal accounts after a 10-year banking relationship,” Cullen said. “They even closed my three-year-old son’s college savings account.”

All of that being said, many within the industry believe the full repeal of prohibition, and thus resolution of this particular issue, is closer than ever. Until that happens though, cannabis businesses will continue to lend new meaning to the term “tenacity” as they build successful enterprises in the face of this lofty challenge.

Becky Olson can be reached at beckyo@mjbizmedia.com