Cannabis advertising giant Weedmaps hopes to boost its revenue over the next three years by a whopping 175% – and investors are wagering the California-based company can deliver on that goal.

Since announcing its acquisition of Weedmaps on Dec. 10, Silver Spike Acquisition Corp. has seen its shares more than double, resulting in a Weedmaps valuation at 21 times sales and 98 times EBITDA for 2020.

The stock – which trades as SSPK on the Nasdaq – climbed another 22% after the company filed a Form S-4 with the U.S. Securities and Exchange Commission on Jan. 19, which included audited financials and more detail about the deal and company operations.

Silver Spike Acquisition Corp. plans to take Weedmaps public on the Nasdaq through the deal. So why are investors bidding up the price of the blank-check acquisition company?

In Weedmaps, investors see a profitable, high-margin, fast-growing ad tech and software business that happens to be tied to cannabis sales – but one that does not touch the plant.

Not touching the plant allows the company to enjoy much higher trading volume on the Nasdaq, be owned by traditional investment institutions and avoid IRS Section 280E to pay typical business tax rates.

Besides being one of the few investments providing U.S. cannabis exposure without touching the plant, Weedmaps has an attractive growth story – assuming it can execute its plans to both raise prices and increase its number of clients.

Paying for growth

The market is not valuing Weedmaps on 2020 estimates but, rather, is looking toward the growth projections through 2023.

| Weedmaps Revenue, EBITDA and Valuation (USD millions) | |||||||||

| 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

| Revenue | $ 43 | $ 61 | $ 90 | $101 | $144 | $160 | $205 | $300 | $440 |

| % Growth y/y | 56% | 42% | 48% | 12% | 43% | 11% | 28% | 47% | 47% |

| EBITDA | $13 | $10 | $19 | $15 | $6 | $35 | $50 | $80 | $130 |

| % Growth y/y | 30% | 16% | 21% | 15% | 4% | 22% | 24% | 27% | 30% |

| Margin | 30.2% | 16.4% | 20.8% | 15.2% | 4.2% | 21.9% | 24.5% | 26.8% | 29.5% |

| Pro forma enterprise value / sales | 21.4 | 16.7 | 11.4 | 7.8 | |||||

| Pro forma enterprise value / EBITDA | 97.7 | 68.2 | 42.5 | 26.3 | |||||

| Source: Company documents and MJResearchCo.com | |||||||||

At its Jan. 20 close of $22.28, Weedmaps had a pro forma $3.7 billion market capitalization and a $3.4 billion enterprise value (which excludes $324 million of net cash, though this will be used on acquisitions).

The question for investors is whether the tech company can meet or exceed these aggressive growth targets – whether based on the actual results of 2020 or the 2023 estimates the company provided in December.

If it does, the narrative holds, and the valuation can expand.

If Weedmaps misses, especially on revenue, that will call into question the growth narrative, and the valuation will shrink.

So how does Weedmaps plan to grow revenue 175% over the next three years?

Increasing clients through market share gains

Weedmaps’ business model generates revenues from “paying clients,” or individual dispensaries and businesses, which might be part of larger organizations. A single client might have multiple listings.

In September 2020, Weedmaps had 4,171 clients paying $3,678 per month each, which annualizes to a run rate of $185 million.

To grow revenue 28% in 2021 and 40% each in 2022 and 2023, the company will need to increase the number of clients and/or increase the revenue from each client. Weedmaps says it plans to do both.

Based on MJResearchCo estimates of new retailer growth of 6% in 2021, the bulk of the growth will have to come through growing revenue per client and market share gains by converting existing dispensaries that are not already Weedmaps clients.

Pricing power in featured listings

Weedmaps said it would raise the price on its base monthly subscription prices by 18% for retailers (to $495 from $420) and 34% for delivery clients (to $395 from $295) as of Jan. 1.

However, this translates to revenue growth of only 2%-3%, so there’s a lot more work to be done.

The bulk – 76% – of Weedmaps’ revenue comes from its featured listings.

Like Google’s business model, featured listings let retailers and brands pay more to have their listings highlighted and competitively bid up for traffic.

Weedmaps believes these listings, with an average cost per click of 50 cents per listing, are underpriced compared to their value, so the company is shifting to “performance-based” pricing.

It is also testing a self-serve bidding engine in Colorado and Michigan to sell featured listings on a cost-per-click basis.

Assuming these tests go well, this model will be expanded elsewhere, and Weedmaps customers will need to budget for increasing advertising costs.

To hit the targets, the company still will need to increase the customer base.

Value proposition increases with local competition

MJResearchCo’s research shows that Weedmaps’ value proposition for clients is highly dependent on both the geography and level of competition among retailers in that area.

Once enough retailers are using Weedmaps, the rest will need to join to maintain their market share.

Reflecting this dynamic, Weedmaps has penetrated 80%-100% of the fragmented California market (which accounts for 50% of the company’s revenue) but less than 50% of the rest of the U.S.

Small, single-unit operators without their own brand or scale receive the biggest benefit from advertising on Weedmaps.

Weedmaps has penetrated about a quarter of the retailers controlled by the larger publicly traded multistate operators, which typically operate in more limited-license states and have the resources to invest in their own loyalty programs, brands and traffic drivers.

In between these two categories are the large single-state operators, which, on average, list about half their stores on Weedmaps. Their stores that are listed on the platform typically are located in tourist destinations with transient customers who might be unfamiliar with the local brand.

Growth with MSOs with rising competition?

So the question becomes: Will the U.S. market overall evolve to look more like California, with lots of fragmented operators, or will Weedmaps be able to penetrate large operators?

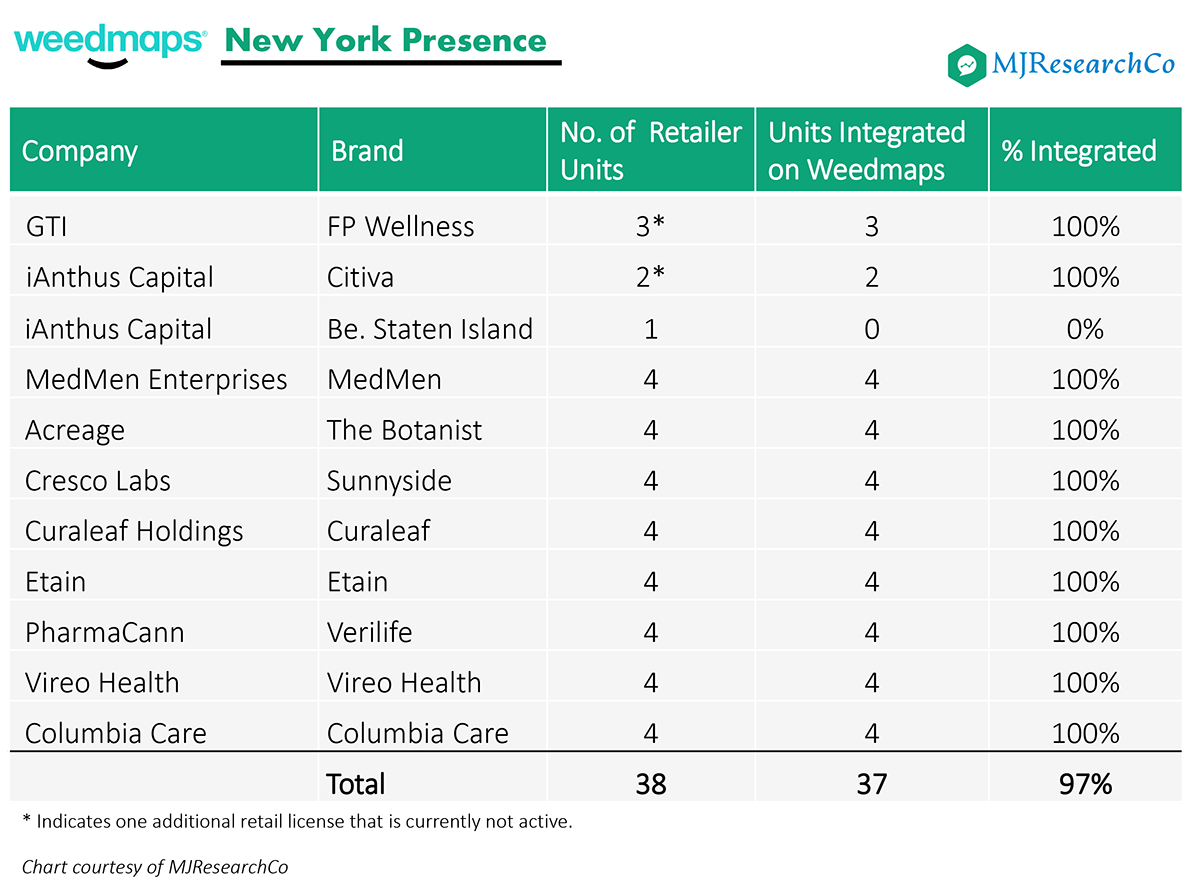

It depends. By our count, Weedmaps has 37 dispensary listings in New York – out of a total of 39 dispensaries, according to the 2020 Marijuana Business Factbook.

MSOs control most of those locations.

It appears that if the market is competitive or there is a lack of market dominance, MSOs will use Weedmaps.

Conversely, concentrated markets such as Florida show lower adoption. Trulieve lists only eight of its 68 dispensaries on Weedmaps. Curaleaf lists none of its 33, while Green Thumb Industries has four of its six on the platform.

Customer churn risks to price increases

In any competitive business, the risk is that price increases can be large enough to cause customers to churn to competitors or alternatives.

Weedmaps does not operate in a vacuum. It has direct competition from Leafly, Dutchie, Jane Technologies and LeafLink.

Changing laws might bring more mainstream competitors as well, such as Google.

Finally, there is the question of which brand has the real power: the client’s or Weedmaps’?

“54% of our users we survey can’t even name a favorite brand,” Weedmaps CEO Chris Beals said on a December conference call.

It will ultimately come down to the company’s pricing power and just how “must-have” the service is to dispensaries.

With the competing goals of increasing clients and charging them more, Weedmaps has its work cut out. Fortunately for the company, it will be helped by a macro tailwind of increasing cannabis consumption and expanding legalization.

The data used in this analysis comes from the company’s presentation and conference call on Dec. 10, 2020, and the Form S-4 filing from Jan. 19, 2021, all of which can be viewed on the SEC website.

Mike Regan is the founder of MJResearchCo.com and a regular contributor to Marijuana Business Daily. He and fellow analyst Colin Ferrian can be reached at mikeandcolin@mjresearchco.com.