The days of $100 million-plus golden parachutes in the United States might be over.

But the phenomenon of rewarding CEOs with hefty payouts remains alive and well in mainstream merger and acquisition deals and has taken root in the marijuana industry.

An MJBizDaily examination of recent marijuana M&A deals reveals a variety of ways that CEOs of acquired cannabis businesses will net millions of dollars in the transactions – over and above the premium paid for their companies’ stock.

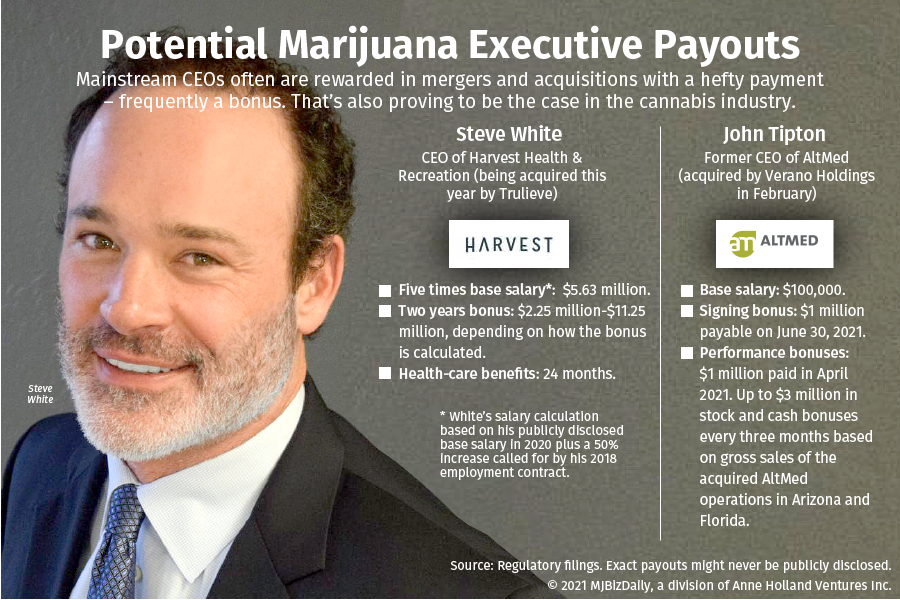

Steve White, CEO of Arizona-based Harvest Health & Recreation, which is being acquired by Florida-based Trulieve in a deal initially valued at $2.1 billion, stands out.

He has “change of control” provisions that could generate a payout well in excess of $10 million. (See graphic above.)

By contrast, John Tipton, CEO of Florida-based AltMed, which was acquired by Illinois-based Verano Holdings in February, doesn’t have a generous change-of-control provision.

But Tipton’s deal with Verano did include some sweeteners: He received a $1 million signing bonus and nets up to $3 million a quarter via a cash and stock bonus based on the financial performance of AltMed’s acquired operations in Florida and Arizona, according to regulatory filings.

Then there’s the stock reward.

When Trulieve announced its blockbuster deal in May to acquire Harvest, the merger conversion rate represented a 34% premium for Harvest stockholders.

“Usually the big payoff from these (merger and acquisition) deals is the acquisition premium,” said Fred Whittlesey, a marijuana compensation expert who is founder of Seattle-based Compensation Venture Group.

The deal premium narrowed to 3% as of Aug. 6, mostly reflecting a decline in Trulieve’s share price but also an increase in Harvest stock price since the deal was announced. Trulieve stock trades as TCNNF and Harvest as HRVSF, both on the over-the-counter markets.

“This (the narrow premium) basically means the market is getting pretty confident that the deal will go through,” said Mike Regan, founder of Denver-based MJResearchCo.com and a contributor to MJBizDaily and MJBizFinance.

White beneficially owns Harvest stock worth $91.7 million, based on the Aug. 6 market close, Regan calculated.

Beneficial ownership means White controls that holding, but some could be owned by other members of his family, or other investors. The details aren’t disclosed.

Based on the merger conversion rate, those shares would be worth $94.6 million in Trulieve stock if the merger had closed Aug. 6, Regan said.

Lack of transparency

Here’s the thing about the M&A deals: Investors might not know exactly what the CEOs of the acquired companies receive in payouts unless the figures show up in future regulatory filings such as proxy statements in advance of annual shareholder meetings.

White’s agreement is especially fuzzy. And Trulieve likely won’t be required to disclose his final payout unless he stays on as an executive of the company.

White’s change of control provisions or merger payout are as follows:

- Five times his base salary.

- Two years of bonuses.

It’s unclear from the regulatory filings, however, what White’s base salary will be for the payout, and how the bonuses are calculated.

Harvest didn’t respond for comment.

Lynn Ricci, Trulieve’s director of investor relations, told MJBizDaily via email that “this is not public information so we cannot comment, especially given Harvest’s upcoming shareholder vote and while there are regulatory approvals pending.”

White stands out because he consolidated control of Harvest in March 2020 through a voting-share exchange with then-Harvest Executive Chair and M&A head Jason Vedadi, Regan noted.

White controls 52% of Harvest’s vote through super-voting shares, according to a proxy statement filed with the U.S. Securities and Exchange Commission in advance of the Aug. 11 shareholder vote on the Trulieve merger.

In other words, White alone has the power to approve the Trulieve deal. He doesn’t need a single additional shareholder to do so.

White has majority voting control even though he beneficially owns only 5.84% of the company’s stock, according to the proxy statement, less than Vedadi’s 7.86% and investor and Harvest board adviser Daniel Reiner’s 9.14%.

Why White wants to sell out now

Harvest has a $100 million convertible note due in May 2022. Refinancing the note could mean raising additional equity that could potentially dilute White’s voting share to below 50%, Regan said.

“Put yourself in Steve White’s shoes,” Regan told MJBizDaily.

“You can risk losing control of the company, or you get frontloaded (change-of-control) benefits and swap Harvest shares for Trulieve shares at a premium that are far more liquid to sell.”

And, Regan added, White winds up “owning a piece of a larger entity where the combination is more valuable together than apart.”

The ultimate size of the change-of-control payout will depend on how White’s salary is calculated.

A 2018 employment contract called for White to receive eye-popping 50% increases in base salary from $500,000 every year.

“50% guaranteed salary increases,” said Whittlesey, a compensation expert for three decades. “I’ve never seen anything close to that.”

“I’ve never seen a 50% annual salary increase not tied to performance,” Regan agreed.

Based on that 2018 employment agreement, White’s $500,000 base salary in 2018 increased to $750,000 in 2019 and should have increased to $1,125,000 in 2020 and to $1,687,500 in 2021.

However, White’s 2020 base salary was listed as $750,000 in a regulatory filing earlier this year.

Harvest didn’t respond to a request for comment to explain why White’s salary was listed as $750,000 rather than $1,125,000 as called for by his 2018 employment contract.

For that reason, though, MJBizDaily set White’s payout calculation at five times $1,125,000, reflecting a 50% salary increase from 2020 to 2021.

But if Harvest is following the 2018 employment contract, White’s 2021 base salary is now $1,687,500 and his payout on salary alone would be nearly $8.5 million rather than $5.63 million.

The two years bonus also is murky.

White’s 2018 employment contract calls for him to receive:

- An annual 100% bonus for “threshold performance.”

- A 300% bonus for “target performance.”

- A 500% bonus for “superior performance.”

But the financial metrics that trigger those bonuses aren’t disclosed in the regulatory filings.

So the graphic above shows a range of what White might earn for two years bonus based on a $1,125,000 base salary: $2.25 million to $11.25 million.

White could be earning a higher salary than that, or the payout could be based on his 2022 salary – both of which would mean a much higher range for his bonus.

Regulatory filings also refer to a “lockup” provision that restricts when and how much White can sell.

“Even if there was no lockup, he couldn’t sell all his shares tomorrow,” Regan said.

Rather, Regan said, it would take months for White to sell his Harvest shares given the liquidity of the stock, which is a function of the volume of buyers and sellers in the market.

But Trulieve’s stock, Regan said, was “six times more liquid” than Harvest’s stock before the deal and would make large stakes easier to sell. That serves as another compelling reason for White to do the Trulieve deal, he said.

Whittlesey said the agreement looks like White’s options also will get swapped out for Trulieve options.

He said Trulieve won’t have to disclose specifics, though the company will make sure the exchange is neutral economically to White.

For example, “if he’s up to $1 million in value today on options, Trulieve will make sure he’s $1 million up” in Trulieve options.

Jeff Smith can be reached at jeff.smith@mjbizdaily.com.