Frank Colombo

Mergers and acquisitions in the marijuana industry are up slightly on a global basis so far this year, while cannabis companies have been raising less money from investors.

Typically, cannabis M&A and funding move in the same direction – but not this year.

What’s going on?

Here is a closer look at this apparent disconnect:

1. Global M&A is at record levels, and the U.S. is not far off the pace.

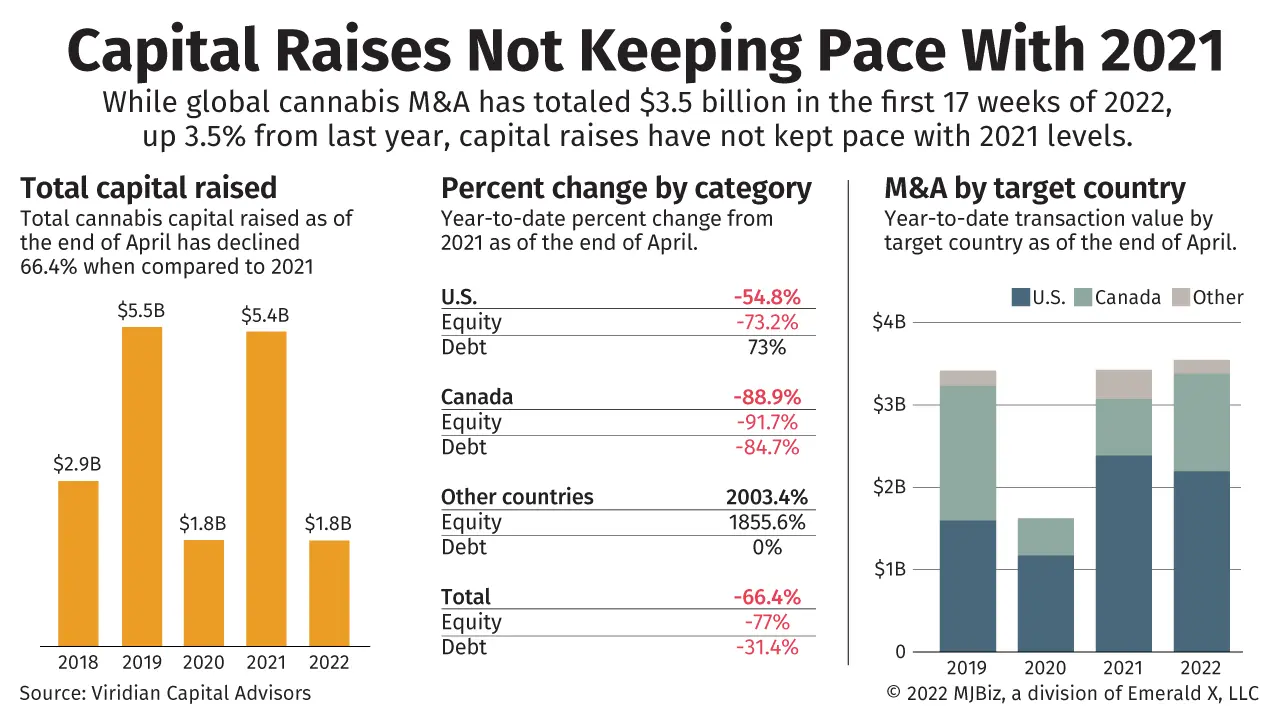

Viridian Capital Advisors has tracked 75 M&A transactions globally with a total value of $3.5 billion through the end of April 2022.

That’s up 3.5% from the same year-to-date period in 2021, the previous peak year since 2018.

M&A in the United States is somewhat weaker, down about 8% year-to-date, to $2.2 billion, versus a record $2.4 billion for the same period in 2021.

The U.S. figures will get a lift when major acquisitions – including Verano Holdings’ purchase of Goodness Growth and Cresco Labs’ acquisition of Columbia Care – close.

2. Capital raise activity is down significantly.

Global equity raises have declined 77% year-to-date, to $962.1 million, with particular weakness in Canada, which is off 92%, to $103.3 million.

By contrast, debt financing is up 73% year-to-date in the U.S., to $729.3 million. But worldwide. it is down 31%, to $863.0 million, because of much weaker results in Canada.

Some critical sectors such as cultivation are down even more sharply – off 78% versus the same period a year ago.

3. Historically, these two segments of the cannabis capital markets generally move in tandem.

For example, in calendar year 2020 – often referred to as the year of the capital crunch – global capital raises were down 64% from 2019 and M&A transactions were off 44%.

In calendar year 2021, however, global capital raises were up 166% over 2020 and M&A was up 572%.

M&A deals got a significant boost last year from global pharma company Jazz Pharmaceutical’s purchase of U.K.-based GW Pharmaceuticals and the megamerger combining Canadian cannabis producers Tilray and Aphria.

Subscribe to the MJBiz Factbook

Exclusive industry data and analysis to help you make informed business decisions and avoid costly missteps. All the facts, none of the hype.

What you will get:

- Monthly and quarterly updates, with new data & insights

- Financial forecasts + capital investment trends

- State-by-state guide to regulations, taxes & market opportunities

- Annual survey of cannabis businesses

- Consumer insights

- And more!

4. Why the two have disconnected recently.

M&A has been robust for several reasons:

- The enormous gap in enterprise value/EBITDA multiples between large and small companies made it easy for acquisitions to be accretive. Big companies didn’t have to care so much that their primary acquisition currency (their stock) was down because the equity prices of their targets were down even more. Smaller companies faced a much higher cost of capital that made it more challenging to grow, and many of them acquiesced to being acquired.

- Acquisition targets have been happy to accept multistate operator stocks at current discounted levels because they perceive significant upside.

- Multistate operators have found it easier to enter new markets by acquisitions rather than building from scratch.

- There has been a pickup in public companies buying other public companies, including Verano/Goodness Growth and Cresco/Columbia Care. These acquisitions are driven by long-term strategic reasons rather than financial benefits.

- There is a sense that federal legalization is coming, fueling the acceleration of the industry consolidation.

5. Why financing is down.

- The 40% year-to-date decline in equity prices has significantly impacted stock issuance. No chief financial officer wants to issue stock at a price below intrinsic value.

- The ups and downs of legalization maneuvering have frozen capital raises. If you perceive a possibility of regulatory change that would materially reduce your cost of capital, you would want to wait to raise money if you could

- Debt costs have come down, and debt issuance is up in the U.S. primarily because the top tiers of American MSOs have become solidly EBITDA positive. Canadian debt is down because Canada’s licensed producers lag in profitability to support debt.

- However, the most important fact is that – according to analysts’ cash-flow estimates for 2022 and 2023 – the large MSOs are already well funded. Cash balances are high, and 2022 and 2023 expectations are for positive free cash flow

6. We believe the current disconnect between robust M&A activity and weak financing activity is likely to continue.

Financings might pick up, but the megadeals of 2021 are unlikely to return. We also expect transformative M&A transactions to continue.

Frank Colombo is director of data analytics at Viridian Capital Advisors, a New York-based cannabis capital, M&A and strategic advisory firm. He can be reached at fcolombo@viridianca.com.

To be considered for publication as a guest columnist, please submit your request here.