Financially strapped MedMen Enterprises is showing modest improvement, raising the possibility that the California-based multistate marijuana operator has hit bottom and is beginning to benefit from its restructuring and turnaround plan.

But huge challenges remain, including a high debt load, ongoing losses and a small cash cushion.

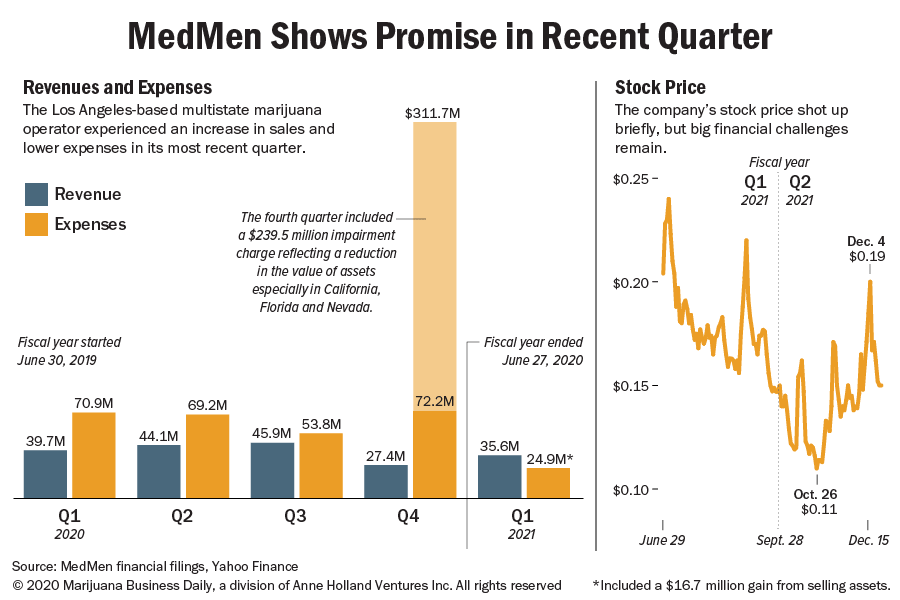

The good news: MedMen’s sales hit $35.6 million in the company’s fiscal 2021 first quarter ended Sept. 26, up from $27.4 million in the previous quarter.

Gross margins also increased and expenses declined in part because of cost control and workforce cuts over the past year or so.

Net losses totaled $32.8 million, but that was down sharply from an $87.4 million loss during the same period of 2019.

MedMen’s interim CEO called the results “transformational.”

But analysts remain cautious.

“Despite the improvement, (MedMen’s) cost structure is still bloated and a heavy debt burden may force management to seek dilutive solutions,” New York investment firm Cowen wrote in a research note.

Pablo Zuanic, a research analyst for Cantor Fitzgerald in New York, had a similar take.

“MedMen sales bounced back in the September quarter,” Zuanic wrote. But the company’s debt load is high, and the “risk of further dilution remains high.”

Embattled co-founder Adam Bierman stepped down as MedMen’s CEO in late January and surrendered his voting control.

Less than two months later, MedMen retained a management advisory firm to help it restructure.

Under a new leadership team, MedMen recently took a $235.9 million impairment charge. The company attributed that charge primarily to a decline in the value of its assets in California, Florida and Nevada.

That, and ongoing losses, have resulted in a negative shareholder equity of $192.3 million for the quarter ended Sept. 26.

Like other companies in similarly poor financial shape, MedMen has included the obligatory boilerplate language in its public filings with securities regulators about the “substantial doubt” that it will survive more than a year as a going concern.

That’s followed by the reasons the company believes it will survive:

- Restructuring plans are in place.

- The company is raising capital.

- Debt agreements have been amended.

- Noncore assets are being sold.

The company’s stock price briefly went up on the news in early December of stronger sales for the quarter but has dipped again to around 15 cents a share.

The company trades on the Canadian Securities Exchange under the ticker symbol MMEN and on the U.S. over-the-counter markets as MMNFF.

MedMen’s debt load is massive, equivalent to 3½ times its annual sales when counting leases, according to Zuanic.

He noted MedMen ended the latest quarter with $498 million in net debt when counting notes payable, convertible bonds and financing and operating leases.

MedMen didn’t respond to a Marijuana Business Daily query for comment.

But in a news release announcing the company’s first-quarter results earlier this month, interim CEO and restructuring officer Tom Lynch said that the quarter “was a transformational one for the company as we grew revenue, improved profitability across our retail footprint and strengthened our balance sheet.

“With the strength of our team and support of our capital partners, we are ahead of schedule with respect to our turnaround plan.”

The company has a little more than two dozen active retail locations in Arizona, California, Florida, Illinois, New York and Nevada, according to the MedMen website.

What looks bright

While most MSOs have benefited from the COVID-19 pandemic by way of greater sales, MedMen actually was hurt last spring when Nevada imposed a strict lockdown, closing casinos and allowing cannabis retailers to offer only home delivery. Curbside pickup was later allowed.

But in the most recent quarter, MedMen’s Nevada sales picked up, and there were other bright spots, according to Cowen:

- MedMen enjoyed strong growth from its store in Oak Park, Ill., with annualized sales of around $15 million.

- The company generated $20.7 million from its 11 California stores, for an annualized rate of $7.5 million a store.

MedMen operates in some of the most potentially lucrative markets in the country, but many of those investments haven’t yet paid off. The latter explains the recent impairment charge.

For example, in 2018 MedMen paid a whopping $53 million to buy a Florida cultivator with a vertical license.

MedMen now has 10 dispensary permits in Florida’s fast-growing medical cannabis market. But to date, MedMen has been able to carve out only about a 1% market share, according to state data.

In New York, MedMen has one of only 10 vertical medical cannabis licenses in a state that could legalize adult-use marijuana as soon as 2021. But sales are modest from the company’s four dispensaries in the state.

MedMen also has shed operations in promising markets.

- The company sold medical marijuana assets in Arizona, which recently legalized adult use.

- MedMen also disclosed that it recently sold a license in Evanston, Illinois, for $20 million, with $10 million paid so far.

- In June, Virginia regulators voted to rescind MedMen’s medical cannabis dispensary license in a state seen as attractive because of a limited-licensing structure and prospects for adult-use legalization.

Bierman overhang?

Before Bierman’s departure, lawsuits against MedMen were piling up.

MedMen notes in its regulatory filings six pending lawsuits, including one that’s in arbitration.

Allegations include misrepresentation of a financial transaction and breaching a contract with the company’s former chief financial officer.

Claims from these lawsuits run into the millions of dollars.

But MedMen hasn’t set aside any money for potential losses.

In its most recent quarterly filing, the company states: “As of September 26, 2020, there were no pending or threatening lawsuits that could be reasonably assessed to have resulted in a probable loss to the company in an amount that can be reasonably estimated.”

Even if the lawsuits don’t result in large financial damages, MedMen will continue to incur legal expenses defending the lawsuits.

MedMen also has continued to incur expenses related to Bierman.

The company paid Bierman total compensation of $959,233 for the fiscal year ended June 27, according to a company proxy filed in October.

In addition, Bierman received estimated benefits of $890,561 for “executive protection” and $106,183 for a car lease and insurance.

The executive-protection expenses weren’t detailed in the proxy, but such services typically can include bodyguards, home security systems, private jet travel and even background checks for other employees.

The proxy noted that MedMen agreed to provide security protection to Bierman for 90 days after his departure and pay for his car lease and related insurance for one year after his departure.

Wait and see

Analysts now are waiting to see if MedMen can continue to grow its sales, cut its expenses and show a path to profitability.

They note that MedMen is likely to open three more stores in California this fiscal year – or four if the company wins litigation over a Pasadena location – in addition to two stores in Massachusetts, one in Illinois and perhaps some in Florida.

But only the store in Illinois is substantially outperforming the market, in Zuanic’s view.

“For a company with supposedly such a known retail banner, sales 14% above the California average is not much, in our opinion,” he noted of MedMen’s California stores.

Then there’s the coronavirus pandemic, which generally has been a plus for marijuana retailers but not so good for MedMen.

The company noted in its most recent quarterly report that it had experienced decreased sales in certain locations in California and Nevada “due to reduced foot traffic as a result of shelter-at-home orders, declining tourism and social distancing restrictions within a retail establishment.”

Last week, Zuanic warned that “near-term risks” are increasing for MSOs because of the coronavirus surge and the possibility of new restrictions.

If so, that could set MedMen back again.

Jeff Smith can be reached at jeffs@mjbizdaily.com