(The map above has been updated to correct the positioning of New York and Pennsylvania.)

(This is the second installment in an occasional series on existing marijuana markets that offer good business opportunities. The previous installment is available here.)

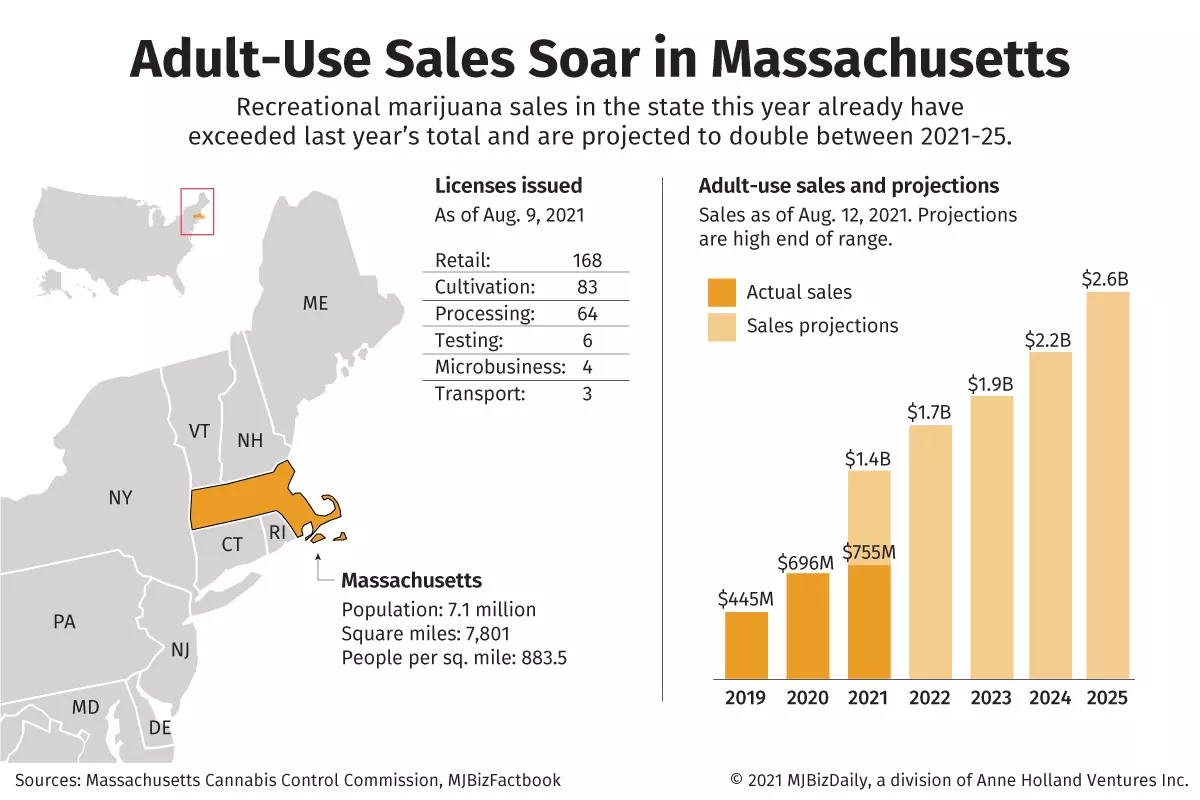

After a slow start in late 2018, recreational marijuana sales in Massachusetts are surging – and on pace to exceed $1.2 billion this year and reach as much as $2.6 billion by 2025.

Cannabis businesses are attracted to a market that is densely populated and a licensing regime that prevents an oligopoly by allowing companies to operate only three adult-use stores and 100,000 square feet of cultivation canopy.

Strong business opportunities remain in cultivation and in select retail locations, including the underserved Boston area. Social equity applicants also have opportunities in marijuana retail and delivery services.

“I think there’s a fair amount of runway left to go in Massachusetts until the market hits full maturity,” said Jesse Alderman, the Boston-based co-chair of Foley Hoag’s nationwide cannabis practice.

But most of the “flags have been planted in the retail market,” Alderman said, noting a “COVID-era explosion” of retail stores with dozens of additional applications in the licensing pipeline.

Massachusetts regulators had issued 168 final adult-use store licenses as of last week, according to the Massachusetts Cannabis Commission open data portal.

While some of those aren’t yet open for business, the numbers compare with 39 stores in operation as of early 2020, according to the 2021 MJBizFactbook.

The recreational marijuana market got off to a slow start after its November 2018 launch in large part because the state mandated what became highly controversial “host community agreements” (HCAs) between municipalities and marijuana businesses.

Marijuana businesses had to negotiate such agreements before applying for their state licenses.

Other hurdles exist today.

According to Alderman, potential new entrants might find it difficult to break into the state’s retail market unless they:

- Are social equity applicants.

- Already have agreements with municipalities.

- Acquire existing retail locations.

Prized retail locations typically command prices of $5 million-$10 million.

Cultivation could offer potential market opportunities in Massachusetts, too.

“What we haven’t seen is a similar explosion of cultivation capacity,” Alderman said. “With sales growing rather robustly, the wholesale market remains constrained and is very favorable to growers.”

That also might change, however, if most applications in the licensing pipeline are approved and facility plans come to fruition.

Why Massachusetts is attractive

Frank Colombo, director of data analytics for New York-based Viridian Capital Advisors, noted that a state’s regulatory environment generally is a key determinant in how attractive it is to new entrants.

In that sense, he said, Massachusetts is a dichotomy.

“It has a huge population and a new recreational marijuana program. That, on one hand, makes it extremely attractive,” Colombo said. “On the other hand, the regulatory regime has been relatively restrictive.

“It’s one of the only states not to classify recreational cannabis as an essential good during the (firsts few weeks of the) pandemic and completely outlawed vaping products for a while (during the 2019 vaping crisis).

“It’s symptomatic of a regulatory regime that hasn’t been very pro-industry.”

Still, in what is a relatively new recreational market, “we already are seeing pretty much all of the multistate operators with one or two exceptions having stakes in Massachusetts,” Colombo said.

MSOs, in fact, are aggressively building out the maximum allowed footprint to take advantage of a dense population and strong demand.

For example, Arizona-based 4Front Ventures this week announced that it won final approval for its third store – in the Boston suburb of Brookline.

MSOs have been part of a flurry of big deals, such as:

- Atlanta-headquartered Parallel, then Surterra Wellness, bought Massachusetts-based New England Treatment Access (NETA) in 2019 for an undisclosed price.

- Illinois-based Cresco Labs announced in March a deal to buy vertically integrated Massachusetts operator Cultivate for $90 million, plus up to $68 million in earnouts based on certain financial targets.

- Florida-headquartered Jushi Holdings announced in April it would buy vertically integrated Nature’s Remedy for up to $110 million.

- Illinois-based Green Thumb Industries acquired Liberty Compassion in June for an undisclosed price. The deal adds two stores and a cultivation and processing facility to GTI’s existing Massachusetts operations.

Smaller merger and acquisition transactions now seem to be the norm in Massachusetts.

For example, in June, Florida-based Trulieve closed on the acquisition of a retail store in Worcester for $13.5 million, including $7 million in cash.

Even Canadian-based and mainstream U.S. companies are eyeing Massachusetts.

Last week, Ohio-based Scotts Miracle-Gro Co. announced a strategic investment in Toronto-based RIV Capital, which is targeting emerging U.S. cannabis markets.

RIV CEO Narbé Alexandrian, in an interview with MJBizDaily, cited Massachusetts as one of the markets the company is interested in.

Retail limited in some areas

What makes the Massachusetts marijuana market hard to penetrate today, Alderman said, is that most municipalities have chosen, through the HCAs, which businesses they want to partner with.

“In many cases, municipalities already have that in the rearview mirror,” he said.

Some municipalities are still open for business, but those include areas where a new entrant could face entrenched competition.

“If you look at a map of the dispensaries, they’re all over the place, stretching to the Berkshires, the western boundary,” Colombo said. “What you don’t see yet is very many in Boston. It’s underserved.”

But getting into Boston and some suburbs is more complicated. For example:

- Boston wants to license one social equity applicant for every non-social equity applicant, Alderman said.

- Cambridge is providing priority to social equity applicants for two years.

- Somerville is focusing on economic equity applicants, locally owned businesses and existing medical cannabis operators.

“I would say they are not officially closed in those jurisdictions, but there are tremendous barriers if you’re not a social equity applicant,” Alderman said.

But there are operators breaking into the underserved Boston market, with big expectations.

Happy Valley, a Massachusetts-based, vertically integrated operator, in June opened its flagship store in East Boston, just minutes from Logan International Airport. Happy Valley also has a store up the coast in Gloucester.

“The potential of Boston’s cannabis market is massive as result of the demographics of the city’s residents coupled with the number of annual visitors for both tourism and business,” Michael Reardon, the company’s chief executive, wrote in an email to MJBizDaily.

Despite efforts to give minorities and other underrepresented communities opportunities in the marijuana industry, Massachusetts has so far fallen short of its social equity goals.

And one big reason is that the state Legislature gave far too much power to municipalities in terms of the host community agreements, Alderman said.

Cannabis companies complained that most municipalities demanded the maximum 3% of gross sales as a community impact fee without evidence of actual costs, plus tens of thousands of dollars of “donations” and other payments.

At one point, federal prosecutors reportedly were investigating some of the deals, and a study paid for by the Massachusetts Cannabis Business Association concluded that cannabis businesses had paid at least $2.46 million in fees more than lawfully allowed under the HCAs.

“I don’t know of any other industry except for gaming that has to pay a legalized extortion fee to open in the community,” David O’Brien, president and CEO of the Massachusetts Cannabis Business Association, told MJBizDaily in 2019.

Legislative fixes have been proposed, such as to clearly cap what municipalities could charge in fees and open up the process.

“The sad truth is that the ship has sailed,” Alderman said. “The damage has been done.”

Jeff Smith can be reached at jeff.smith@mjbizdaily.com.