In the days after the Great Recession (2008-09), the U.S. government implemented a policy of quantitative easing to boost the recovery. In 2010, after the first round of QE, Mike asked Warren Buffett about his views on inflation and investing.

The Oracle of Omaha replied: “Equity in a good business is a claim on future human behavior.”

What this means is that good businesses that provide desired services can raise prices and manage costs to expand profits during inflationary periods. And they can grow earnings more than the decline in the valuation multiples to increase stock prices.

Cannabis investors in most U.S. markets will be able to hedge inflationary repercussions, because unlike most traditional and slower growing industries, this industry has many opportunities to offset increases in input costs, wages and interest rates with secular revenue growth drivers, cost cuts and lower cost capital, allowing for profit expansion to offset any valuation multiple contraction.

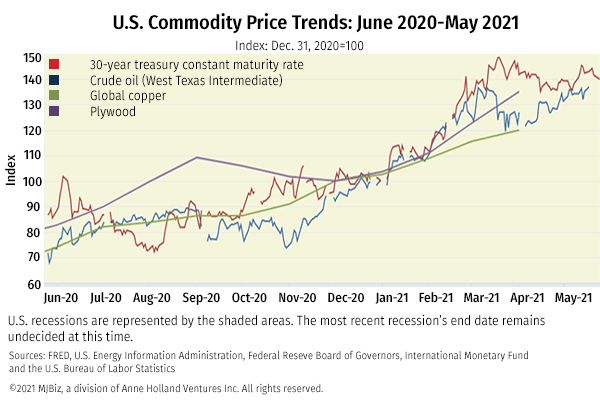

Some context: Year-to-date, the 30-year treasury yield has risen to 2.3% from 1.7%, crude oil is up 35%, copper has increased 29%, corn is up 31%, and in the past year live cattle prices are up 30% and there are reports of spot lumber rising fourfold – all signals of widespread inflation, as shown in the year-to-date chart above (index: Dec. 31, 2020=100).

But putting these moves into a longer-term context, shown in the chart below, the world has seen a chronic decline in interest rates for decades. For example, 30-year treasury rates are still 62% lower than they were in 2000, oil is 40% lower than the shale boom in 2012-2015, and Mike remembers earning 6% in a savings account in 2002 that only pays 0.4% today.

Short term, costs to build new facilities and equipment may rise as producers pass on higher commodity input costs, and higher energy costs could drive up indoor cultivation costs.

But if we enter a long-term inflationary cycle, cannabis is well positioned because the continued federal illegality of cannabis has led to excessive costs that provide cost-cutting opportunities regardless of inflation:

- The cost of capital should decline more than any increase in interest rates driven by several factors including: access to normal banking and broader institutional investment, uplisting to the higher volume public stock exchanges and the potential for convoluted 280E taxes to be changed. Few industries other than cannabis borrow at double-digit interest rates, so at worst, inflation would normalize traditional industries.

- Cannabis typically pays higher rates for labor than traditional industries for similar roles, and increasing social normalization expands the potential labor pool to offset rising wages.

- Payroll processing, credit card processing, rent, insurance and other general and administrative expenses are typically higher in cannabis than those in similar traditional industries. These costs should decline with continued normalization.

Cannabis also has opportunities to improve efficiencies through scale and specialization, tactics already employed by more mature consumer/pharma/industrial sectors. Colin notes that many operators have undefined processes and lack standard operating procedures, leading to salaried cultivation managers staying late to spray crops after the lights have turned off, dispensary teams using their breaks to hand-label inventory, and corporate development teams manually pulling market research data due to a lack of automation and tools.

Vertical integration, either as a legal requirement or by necessity given the lack of a robust supply chain, also causes inefficiencies compared to traditional industries. We expect a similar specialized supply chain to eventually emerge in cannabis as well.

And then there’s pricing.

This is where cannabis splits into micromarkets of differing maturities, and between business models with pricing power and those at the mercy of pricing driven by supply and demand, between both legal and illicit markets.

And if interstate commerce ever comes to pass, significant changes will occur in a national market where wholesale prices range from roughly $1,000 per pound (California) to more than $4,000 per pound (Massachusetts).

– Mike Regan and Colin Ferrian of MJResearchCo. They can be reached at mikeandcolin@mjresearchco.com.

Deal of the Week / In partnership with Viridian Capital Advisors

Making Sense of MedMen’s Moves

Last week, MedMen Enterprises (CSE: MMEN; OTCQX: MMNFF) closed a sale of $10 million of units at $0.32 each. Each unit consists of one Class B subordinated voting share and one warrant exercisable at $0.352 for three years. We value the warrant at approximately $0.05 per unit, giving a net share price of US$0.27 per share, a discount of roughly 16.5% from preannouncement levels.

The deal looks like reasonably good execution for a transaction like this, and the size is unremarkable, so what makes this transaction interesting?

We are amazed that MedMen can access the equity market at all!

The company continues to bleed cash: Cash flow from operations for the quarter ended March 31 was roughly -$14 million, down from -$10 million in the previous quarter.

- Liquidity remains weak: As of March 31, MedMen had negative working capital of $168 million.

- Leverage is extraordinarily high: Total debt to market cap is over 2.7X, a level we associate with deep distress/insolvency.

- On May 11, the company entered into its fifth modification of its loan agreement with Hankey Capital and got a new waiver from Gotham Green Partners.

- MedMen ranks as the worst credit out of the 20 U.S. cultivation & retail companies with a market cap of more than $100 million on the Viridian Credit Tracker ranking system.

So what’s the good news?

- MedMen has managed to keep itself alive by selling ancillary (and some not-so-ancillary) assets and reducing total SG&A expenses.

- The company canceled 97 million in-the-money options owned by Gotham Green because it has had two consecutive quarters of “retail adjusted EBITDA.” We tend to be skeptical of “adjusted EBITDA” in the first place, but MedMen’s measure gave it positive adjusted EBITDA of $7.4 million by eliminating negative cultivation and wholesale gross margins of $4.2 million and corporate SG&A of $16.4 million. Adjusting costs out of the numbers isn’t the same as eliminating them, though it would be nice if it were that easy!

- The best news for MedMen is that it enjoys a captive audience of debtholders who can’t afford to pull the plug. Gotham Green is doing whatever it can to maintain optionality. It holds secured debt in case it is forced to push the button but hopes that legalization will allow it to unload MedMen on somebody else, perhaps a wayward Canadian LP.

And in typical 2021 fashion, the bet seems to be working. Since the Georgia Senate flip, MedMen stock significantly outperformed our basket of 25 cannabis stocks. Are we wrong to view this as an out-of-the-money call option on legalization?