(This story has been updated to correct the name of AeroPay from Arrow Payments.)

Are the days of the cashless ATM in marijuana stores numbered? Possibly.

After credit card giant Visa warned banks and others earlier this month about the misuse of cashless ATMs, several marijuana industry executives now believe retailers will be forced to revert to cash-only sales or to adopt other debit-card payment systems.

That would amount to a logistical headache for potentially thousands of retailers across the nation.

But the fallout could be more severe, according to some industry executives.

They believe criminal charges could be on the way for those involved in helping set up cashless ATMs in marijuana shops.

“This is probably, if I had to guess, the beginning of a much larger effort,” said Tyler Beuerlein, chief business development officer at Arizona-based Hypur, which helps connect marijuana companies with banks.

Beuerlein believes Visa is prepping to shut down every cashless ATM that violates its terms of service, including those being used to facilitate marijuana transactions.

“I think there’s a concerted effort to shut this model down for good,” Beuerlein said, adding that the shutdowns could begin at any time.

That has some retailers and their partners thinking about how to pivot – and how to cover themselves legally – if they do lose the use of cashless ATMs, said Sundie Seefried, the president and CEO of Colorado-based Safe Harbor Financial.

“What we’re doing is sending a mailing to all our cannabis clients saying, ‘Here’s the notice, you need a backup plan, you need to consult with legal and figure this out, and we have to figure this out because they’re telling us to,'” said Seefried, who predicted cashless-ATM shutdowns will start by the end of February at the latest.

What happened and what’s next

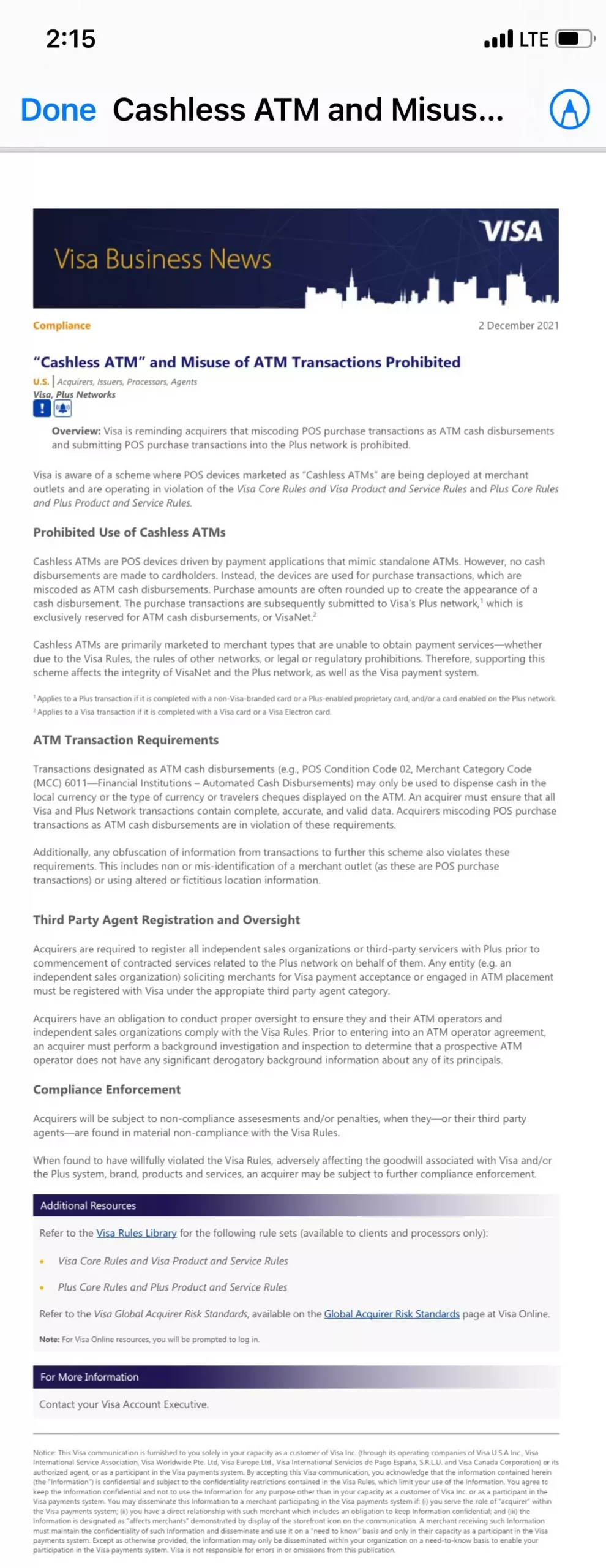

On Dec. 2, Visa sent a letter to banks and other financial partners saying it was aware of a “scheme” in which cashless ATMs were being deliberately miscoded to disguise the true nature of the transaction.

On Dec. 2, Visa sent a letter to banks and other financial partners saying it was aware of a “scheme” in which cashless ATMs were being deliberately miscoded to disguise the true nature of the transaction.

In particular, cashless ATMs used for cannabis purchases are miscoded as ATM cash withdrawals.

“They are referred to as ‘cashless’ because the cardholder receives product instead of cash,” Denver-based cannabis technology firm Akerna noted in a recent news release.

Visa warned that violators of its terms would be subject to unspecified “penalties” and “compliance enforcement.”

While Visa did not specifically cite the marijuana industry in its letter, industry executives took it as a warning that the financial behemoth is eyeing cashless ATMs in use at cannabis shops across the U.S.

Akerna estimates that half of all cannabis stores across the nation use cashless ATMs – meaning thousands of retailers.

The MJBizFactbook estimates there are 7,200-8,800 stand-alone marijuana retail shops nationwide, on top of 2,700-3,300 stores operated by vertically integrated businesses.

Over the past several years, cashless ATMs have become a commonplace payment method at retail shops – despite the federal prohibition targeting marijuana and the general lack of banking services for many MJ companies.

So what’s next for Visa?

“If I had a best guess, I’d say that Visa’s first shot off the bow is the statement,” Beuerlein said.

“And in past examples of them taking a stance like this, I would imagine they would follow up with heavy penalties if they knew what banks were processing these transactions.”

Beuerlein also said Visa is likely to first target banks that have been processing the transactions but that repercussions could reach as far as marijuana retailers.

That would force operators to pivot, either via a return to accepting only cash from customers or to some other type of card payment system.

Seefried agreed that the most likely impact will be the shutdown of cashless ATMs at cannabis retailers within a couple of months.

“Big institutions don’t act that fast, but when they put out a notice like (Visa’s), they’re serious,” Seefried said. “I think this was Visa putting everybody on a courtesy notice.”

Stay informed with MJBiz Newsletters

MJBiz’s family of newsletters gives cannabis professionals an edge in this rapidly changing industry.

Featured newsletters:

- MJBizDaily: Business news for cannabis leaders in your inbox each morning

- MJBiz Cultivator: Insights for wholesale cannabis growers & vertically integrated businesses

- MJBizCon Buzz: Behind-the-scenes buzz on everything MJBizCon

- MJBiz Retail + Brand: New products, trends and news for cannabis retailers, distributors and marketers

- Hemp Industry Week: Roundup of news from hemp farming to CBD product manufacturing

- And more!

Seefried said she doesn’t anticipate criminal charges, despite the conviction this year of two former executives from California delivery company Eaze for tricking banks into processing credit card payments, a situation that seems eerily similar to the subject of Visa’s warning.

“In this case … it was still a gray area. It’s different than going to the banks and straight out lying to them,” Seefried said. “I think Visa is looking for cooperation here. And clients.”

Concerns overblown?

But Todd Kleperis, the founder of Florida-based Payzel, another financial services firm in the cannabis space, said he doubts very much that will happen because shutting down so many cashless ATMs could cost Visa billions in revenue.

“Practically, I don’t think that will happen, because they could do that, but then they’re going to lose a lot of their own volume. And Visa isn’t going to cut off their nose to spite their face,” Kleperis said.

“They’re going to wean it away, maybe whack some of the bigger companies so everyone else kind of shudders, but I doubt they’re just going to turn it all off.”

So far, MJBizDaily has not learned of any retailer whose cashless ATM has been shut down since Dec. 2.

But Beuerlein said it could happen at any point within “weeks, maybe a couple months.”

There is precedent for such action. In 2014, hundreds of retailers in both Colorado and Washington state lost access to their cashless ATMs, and in 2019, it happened to some licensed marijuana shops in San Francisco.

Los Angeles-based attorney Joe Rogoway predicted a “gradient of outcomes” for the various players involved in the cashless ATM “scheme.”

Rogoway said criminal charges could potentially be filed if some of the businesses that fooled Visa into processing transactions at marijuana retailers were found to have used “false companies” to essentially defraud Visa.

But Rogoway noted it’s almost inconceivable at this point in history – with the majority of the U.S. having already legalized medical marijuana – that Visa itself will face any blowback from federal bank regulators for having engaged in marijuana commerce, even by accident.

Which means it’s also unlikely Visa will push for criminal charges to be filed against operators that fooled it into helping marijuana retailers accept card payments from customers, Rogoway said.

“The criminal liability is not something that Visa needs to worry about,” he said. “And if they don’t need to worry about that, then what is this really all about and what are they really trying to protect against?

“In some ways, it’s a farce, because no one is going to indict Visa.”

Rogoway predicted that, “by and large, what is mostly going to be experienced is a lot more hassle for the businesses, a lot more hassle for the consumers, no real change in business operations other than that.”

“The company that is going to feel this the most is going to be Visa,” he added, “because they’re going to be losing out on billions of dollars in sales for really no good reason.”

What can be done?

Seefried said the best action retailers can take now – if they have a cashless ATM – is to prepare to pivot.

She also said there are several replacement options already on the market that could replace cashless ATMs and still allow marijuana shops to accept debit cards such as CanPay and AeroPay.

“There are options,” Seefried said.

Rogoway agreed that any marijuana retailer using a cashless ATM should consult with an attorney, because another potential outcome to be avoided at all costs is getting blacklisted by Visa.

Such a result, he said, could be “catastrophic” for any business that is hoping to survive until federal legalization actually happens.

Being blacklisted would remain a major handicap, if not a death knell, once legalization transforms the industry landscape and opens the doors to the banking universe for cannabis companies, he said.

John Schroyer can be reached at john.schroyer@mjbizdaily.com.