Public health insurance reimbursements for cannabis in Germany have fallen for the second straight quarter.

Unless this drop is being offset by an increase in private prescriptions, it means that total sales of medical cannabis in Germany – Europe’s largest market – are decreasing. (Data for private prescriptions is not available.)

It is the first time reimbursements have fallen for two consecutive quarters since the medical program started in early 2017, according to new data for the period ended Sept. 30.

The cannabis flower category is declining both in terms of the number of prescriptions and the total euros reimbursed by statutory health insurers.

This means companies with business plans based on projected exponential growth should check their premises and adapt to how the market is evolving in reality.

In the third quarter of 2020, reimbursements of medical cannabis and cannabinoid-based medicines totaled 36 million euros ($43.8 million), according to the German National Association of Statutory Health Insurance Funds (GKV-Spitzenverband).

That is 2% lower than the previous quarter.

German pharmacies processed 82,986 prescriptions under the statutory program in the quarter ended Sept. 30.

That’s 3% more than the previous quarter.

However, the average value per prescription dropped 5%.

Reimbursed flower fell from 20 million euros the first quarter of the year to 17.6 million euros and 16.8 million euros in the second and third quarters, respectively.

The extracts category experienced timid growth in the third quarter over the previous quarter.

Flower reimbursements are still larger than those of compounded extracts.

The current trend indicates that might flip in 2021.

In November, Marijuana Business Daily warned that sales strategy is vital at this stage of the German flower market.

What’s included

All medical cannabis and cannabinoid-based products are included in the data, from unprocessed flower to finished pharmaceutical products such as Sativex and Canemes.

The only exception is Epidiolex reimbursements, which are excluded from the data provided by the GKV.

MJBizDaily previously reported that statutory health insurers have approved more than 60,000 applications for reimbursement since March 2017.

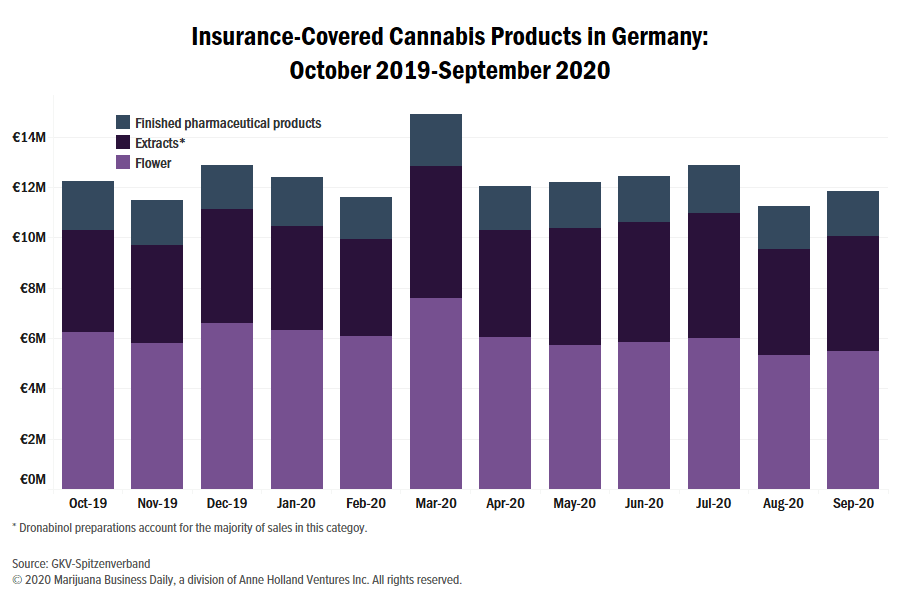

March 2020 was the strongest month since the current regulatory framework was implemented in 2017, with reimbursements reaching almost 15 million euros, an increased most likely spurred by the onset of the COVID-19 pandemic.

GKV-reimbursed cannabis since April has remained stable, coming in between 11 million euros and 13 million euros each month, or about the same as the end of 2019.

As noted above, this data does not include private prescription sales. These are paid out of pocket by patients who have GKV insurance but have not qualified for cannabis coverage or potentially covered by private insurers.

Because GKV reimbursement data does not include private prescriptions, the total sum covered by statutory health insurers should not be considered as the total market size.

The German government acknowledged earlier this year it does not know how much cannabis is sold through private prescriptions.

All reimbursement data is based on retail prices at pharmacies, which are the only authorized points of sale for patients in Germany.

For products not included in the “finished pharmaceutical products” category, pharmacies previously marked up prices as much as 100% from wholesale.

But that changed, retroactive to March 2020, with margins slightly compressed across the supply chain.

Lower prices, more extracts, less flower

The average prescription value – which stands at 434 euros – decreased across the board by 5% on average, with the 7% decrease for compounded extracts representing the largest drop.

In other words, the increasing number of prescriptions is not sufficient to overcome declining prices.

Compared to the second quarter, flower reimbursements in the third quarter dropped 4% in value while extracts sold as magistral preparations barely grew 1% in terms of euros covered.

The number of flower prescriptions covered by GKV insurers decreased 2% while those for compounded extracts increased 8%.

Reimbursements of finished pharmaceutical products remained unchanged in euros quarter-over-quarter.

While the ratio of reimbursed flower sales to overall sales has been decreasing – from a little more than 50% of the total GKV market at the beginning of the year to 47% in the third quarter – that of extracts has been increasing.

The extracts market is less competitive compared to the flower market, although the extracts segment is gaining new entrants. Recently new products became available both as full-spectrum extracts and isolate.

Within the extracts category, the majority of sales are represented by preparations with pure THC – sold to pharmacies as dronabinol API. But also included are some pharmaceutical CBD sales as well as full-spectrum extracts.

Finished pharmaceutical products, a category represented mostly by Sativex, remained stable, accounting for 15% of the GKV-covered market.

Germany’s domestic flower production is not expected to reach retail shelves until 2021, meaning all flower continues to be imported, either from Canada, the Netherlands, Portugal and, more recently, Spain.

The German cannabis market covered by statutory health insurers is expected to be roughly 150 million euros in 2020, up 22% from 2019.

Alfredo Pascual can be reached at alfredop@mjbizdaily.com